Proposed Revision of Actuarial Standard of Practice No. 27

Selection of Economic Assumptions for Measuring Pension Obligations

STANDARD OF PRACTICE

TRANSMITTAL MEMORANDUM

January 2012

TO: Members of Actuarial Organizations Governed by the Standards of Practice of the Actuarial Standards Board and Other Persons Interested in the Selection of Economic Assumptions for Measuring Pension Obligations

FROM: Actuarial Standards Board (ASB)

SUBJ: Proposed Revision of Actuarial Standard of Practice (ASOP) No. 27

This document contains a second exposure draft of proposed revisions to ASOP No. 27, Selection of Economic Assumptions for Measuring Pension Obligations.

Please review this second exposure draft and give the ASB the benefit of your comments and suggestions. Each written response and each response sent by e-mail to the address below will be acknowledged, and all responses will receive appropriate consideration by the drafting committee in preparing the final document for approval by the ASB.

The ASB accepts comments by either electronic or conventional mail. The preferred form is e-mail, as it eases the task of grouping comments by section. However, please feel free to use either form. If you wish to use e-mail, please send a message to comments@actuary.org. You may include your comments either in the body of the message or as an attachment prepared in any commonly used word processing format. Please do not password-protect any attachments. Include the phrase “ASB COMMENTS” in the subject line of your message. Please note: Any message not containing this exact phrase in the subject line will be deleted by our system’s spam filter. Comments will be posted in the order that they are received. Comments received after the deadline will not be posted.

If you wish to use conventional mail, please send comments to the following address:

ASOP No. 27 Revision

Actuarial Standards Board

1850 M Street, NW, Suite 300

Washington, DC 20036

The ASB posts all signed comments received to its website to encourage transparency and dialogue. Unsigned or anonymous comments will not be considered by the ASB nor posted to the website. The comments will not be edited, amended, or truncated in any way. Comments will be posted in the order that they are received. Comments will be removed when final action on a proposed standard is taken. The ASB website is a public website and all comments will be available to the general public. The ASB disclaims any responsibility for the content of the comments, which are solely the responsibility of those who submit them.

Deadline for receipt of responses in the ASB office: May 31, 2012

Background

The ASB has provided coordinated guidance through a series of ASOPs for measuring pension obligations and determining pension plan costs or contributions:

1. ASOP No. 4, Measuring Pension Obligations and Determining Pension Plan Costs or Contributions;

2. ASOP No. 27, Selection of Economic Assumptions for Measuring Pension Obligations;

3. ASOP No. 35, Selection of Demographic and Other Noneconomic Assumptions for Measuring Pension Obligations; and

4. ASOP No. 44, Selection and Use of Asset Valuation Methods for Pension Valuations.

In January 2011, the ASB issued the first exposure draft of ASOP No. 27. Twenty comment letters were received and reviewed. The comment letters reflected diverse viewpoints and the Pension Committee found them to be helpful; the ASB thanks all those who took the time to comment.

Also in January 2011, the Pension Committee issued a discussion draft of ASOP No. 4. The discussion draft contained a limited number of changes on which the Committee requested input from interested parties. Several comment letters were received and the Pension Committee found them to be helpful; the Committee thanks all those who took the time to comment.

The Pension Committee is continuing its work on several standards. As detailed in the transmittal memo of the first exposure draft of ASOP No. 27, the Committee is focused on the following issues:

- Addressing economic value issues regarding both actuarial methods and actuarial assumptions, thus requiring revisions to both ASOP Nos. 4 and 27, and possibly to ASOP No. 35 as well.

- Coordinating changes to ASOP No. 35 that may be required due to changes in ASOP No. 27 so the two standards provide consistent guidance.

- Developing guidance for the assessment, disclosure, and management of pension risk. The Pension Committee believes that an entirely new standard on risk is the best vehicle for providing such guidance.

- Reviewing ASOP No. 4 in its entirety, not just with regard to economic value issues. This review includes funding methods, contribution policy, funded status, projections, terminology, and valuation of certain types of plan provisions.

- The Pension Committee noted that a review of ASOP No. 6, Measuring Retiree Group Benefit Obligations, was also necessary since ASOP No. 6 incorporates by reference much of the guidance contained in the pension standards. The ASB appointed a new Retiree Group Benefits Subcommittee, under the jurisdiction of the Pension Committee, to address ASOP No. 6.

The Pension Committee has been proceeding on all of these endeavors. At this time, the ASB is issuing the following items:

- Exposure draft of a revision of ASOP No. 4

- Second exposure draft of a revision of ASOP No. 27

An exposure draft of a revision of ASOP No. 6 is expected to be issued in 2012, as well as a discussion draft of a proposed new standard on risk.

Changes to ASOP No. 35 that align with a revised ASOP No. 27 are also likely to be exposed for comment after a revised ASOP No. 27 is adopted. The Pension Committee will take into account comments received on this second exposure draft for ASOP No. 27 before issuing anything for comment on ASOP No. 35.

Key Changes in Second Exposure Draft of ASOP No. 27

Some of the changes in the second exposure draft of ASOP No. 27 introduce new concepts while others are refinements to language in the first exposure draft. Readers are encouraged to review the transmittal memo to the first exposure draft for a discussion of all the changes introduced.

Section Order

A significant amount of text has been reordered in the second exposure draft with the goal of improving the flow of the standard. The reader will see significant reordering of language in sections 3.2 through 3.14.

Reasonable Assumption Standard

The second exposure draft contains a new definition for a reasonable assumption. The first exposure draft considered assumptions to be reasonable if they were not anticipated to produce significant actuarial gains or losses over the measurement period. This approach was consistent with the current definition of “reasonable” used in ASOP No. 35.

The second exposure draft states that an assumption is reasonable if it:

a. is appropriate for the purpose of the measurement;

b. reflects the actuary’s professional judgment;

c. takes into account historical and current economic data that is relevant as of the measurement date;

d. reflects the actuary’s estimate of future experience, the actuary’s observation of the estimates inherent in financial market data, or a combination thereof; and

e. is unbiased (i.e., neither optimistic nor pessimistic), except when provisions for adverse deviation are included and disclosed under section 3.5.1 of this second exposure draft, or when alternative assumptions are used for the assessment of risk.

The Pension Committee felt this principles-based definition was an improvement over the rules-based definition of no gain/loss. The Pension Committee looked at standards from Australia, Canada, and the United Kingdom in developing this definition.

The second exposure draft also contains new language in section 3.6 that acknowledges a range of reasonable assumptions is possible.

Estimates and Observations

The reasonable assumption language in section 3.6 contains some examples on how actuaries might obtain estimates from market observations. The language also states that observations may include estimates of future experience as well as other considerations and that making adjustments to observations may be appropriate.

Geometric and Arithmetic Returns

The second exposure draft continues to draw the actuary’s attention to the fact that investment return expectations are sometimes quoted as forward looking expected arithmetic returns and other times quoted as forward looking expected geometric returns. Section 3.8.3 lists geometric and arithmetic returns as a factor that the actuary should consider in setting an investment return assumption. The second exposure draft does not promote one type of return over the other but does indicate that the actuary needs to understand what type of return is used.

The Pension Committee feels that the revised definition of a reasonable assumption better accommodates assumptions based on both arithmetic and geometric returns.

Appendix 3 contains some background material on arithmetic and geometric returns.

Adverse Deviation (previously titled Conservatism)

Section 3.5.1 of this second exposure draft replaces “Conservatism” with “Adverse Deviation.” One of the challenges with the word “Conservatism” is that it can depend on the viewpoint of the reader. The Pension Committee feels that the term “Adverse Deviation” describes the goal of the standard language better than “Conservatism.”

Rate of Payroll Growth

The Pension Committee added language in section 3.11.3 that discusses an assumption for payroll growth for an entire covered population. The rate of payroll growth for an entire covered population is often different than the payroll growth experienced by an employee who remains in service with the plan sponsor. The actuary will sometimes need an overall payroll growth assumption for cost projections or, in some instances, amortization methods.

Assumption Rationale

The second exposure draft retains the requirement for the actuary to disclose the rationale used in selecting each non-prescribed assumption or any changes made to non-prescribed assumptions. The language has been modified slightly to make it clear that brief rationale statements are sufficient.

Request for Comments

The ASB is issuing a second exposure draft of ASOP No. 27 to provide members of actuarial organizations governed by the ASOPs and other interested persons an opportunity to comment.

The Pension Committee would appreciate comments on the proposed changes and would like to draw the readers’ attention to the following areas in particular:

1. Is the guidance as to a reasonable assumption in section 3.6 clear and appropriate? If not, what changes do you suggest?

2. Are the examples in 3.6.1 regarding market observations clear and sufficient? Is the language regarding observations including estimates of future experience as well as other considerations clear and appropriate? If not, what changes do you suggest?

3. Is the language in section 3.6.2 regarding a range of reasonable assumptions clear and appropriate? If not, what changes do you suggest?

4. Do you agree that the guidance on arithmetic and geometric returns in section 3.8.3(j) is appropriate? Is the language about the proper incorporation of forward looking expected geometric returns into a building block exercise clear?

5. Is the language regarding payroll growth in section 3.11.3 clear and sufficient? If not, what changes do you suggest?

The ASB reviewed this draft and voted in January 2012 to approve its exposure.

Pension Committee of the ASB

Gordon C. Enderle, Chairperson

Mita D. Drazilov, Vice-Chairperson

C. David Gustafson Alan N. Parikh

Fiona E. Liston Mitchell I. Serota

Thomas B. Lowman Judy K. Stromback

Tonya B. Manning Frank Todisco

A. Donald Morgan IV Virginia Wentz

Actuarial Standards Board

Robert G. Meilander, Chairperson

Albert J. Beer Thomas D. Levy

Alan D. Ford Patricia E. Matson

Patrick J. Grannan James J. Murphy

Stephen G. Kellison James F. Verlautz

The ASB establishes and improves standards of actuarial practice. These ASOPs identify what the actuary should consider, document, and disclose when performing an actuarial assignment. The ASB’s goal is to set standards for appropriate practice for the U.S.

Section 1. Purpose, Scope, Cross References, and Effective Date

1.1 Purpose

This standard does the following:

a. provides guidance to actuaries in selecting (including giving advice on selecting) economic assumptions—primarily investment return, discount rate, post-retirement benefit increases, and compensation increases—for measuring obligations under defined benefit pension plans;

b. enhances those provisions of Actuarial Standard of Practice (ASOP) No. 4, Measuring Pension Obligations and Determining Pension Plan Costs or Contributions, that relate to the selection and use of economic assumptions; and

c. enhances those provisions of Actuarial Standard of Practice (ASOP) No. 6, Measuring Retiree Group Benefit Obligations, that relate to the selection and use of economic assumptions.

1.2 Scope

This standard applies to the selection of economic assumptions to measure obligations under any defined benefit pension plan that is not a social insurance program (unless ASOPs on social insurance explicitly call for application of this standard). Measurements of defined benefit pension plan obligations include calculations such as funding valuations or other assignment of plan costs to time periods, liability measurements or other actuarial present value calculations, and cash flow projections or other estimates of the magnitude of future plan obligations. Measurements of pension obligations do not generally include individual benefit calculations or individual benefit statement estimates.

To the extent that the guidance in this standard may conflict with ASOP Nos. 4 or 6, ASOP Nos. 4 or 6 will govern. If a conflict exists between this standard and applicable laws or regulations, the actuary is obligated to comply with the laws or regulations.

If the actuary departs from the guidance set forth in this standard in order to comply with applicable law (statutes, regulations, and other legally binding authority) or for any other reason the actuary deems appropriate, the actuary should refer to section 4.

This standard does not apply to the selection of prescribed assumptions, although the actuary should use the principles set forth in this standard whenever the actuary has an obligation to assess the reasonableness of a prescribed assumption. The actuary’s obligations with respect to prescribed assumptions are governed by ASOP Nos. 4, 6, or 41, Actuarial Communications, which address prescribed assumptions and methods.

Throughout this standard, any reference to selecting economic assumptions also includes giving advice on selecting economic assumptions. For instance, the actuary may advise the plan sponsor on selecting economic assumptions under US GAAP or Governmental Accounting Standards, but the plan sponsor is ultimately responsible for selecting these assumptions. This standard applies to the actuarial advice given in such situations, within the constraints imposed by the relevant accounting standards.

1.3 Cross References

When this standard refers to the provisions of other documents, the reference includes the referenced documents as they may be amended or restated in the future, and any successor to them, by whatever name called. If any amended or restated document differs materially from the originally referenced document, the actuary should consider the guidance in this standard to the extent it is applicable and appropriate.

1.4 Effective Date

This standard will be effective for any actuarial work product with a measurement date on or after twelve months after adoption by the Actuarial Standards Board (ASB).

Section 2. Definitions

The terms below are defined for use in this actuarial standard of practice.

2.1 Inflation

General economic inflation, defined as price changes over the whole of the economy.

2.2 Measurement Date

The date as of which the value of the pension obligation is determined (sometimes referred to as the “valuation date”).

2.3 Measurement Period

The period subsequent to the measurement date during which a particular economic assumption will apply in a given measurement.

2.4 Merit Adjustments

The rates of change in an individual’s compensation attributable to personal performance, promotion, seniority, or other individual factors.

2.5 Prescribed Assumption or Method Set by Another Party

A specific assumption or method that is selected by another party, to the extent that law, regulation, or accounting standards gives the other party responsibility for selecting such an assumption or method. For this purpose, an assumption or method selected by a governmental entity for a plan that such governmental entity or a political subdivision of that entity directly or indirectly sponsors is a prescribed assumption or method set by another party.

2.6 Prescribed Assumption or Method Set by Law

A specific assumption or method that is mandated or that is selected from a specified range or set of assumptions or methods that is deemed to be acceptable by applicable law (statutes, regulations, or other legally binding authority). For this purpose, an assumption or method selected by a governmental entity for a plan that such governmental entity or a political subdivision of that entity directly or indirectly sponsors is not a prescribed assumption or method set by law.

2.7 Productivity Growth

The rates of change in a group’s compensation attributable to the change in the real value of goods or services per unit of work.

Section 3. Analysis of Issues and Recommended Practices

3.1 Overview

Pension obligation values incorporate assumptions about pension payment commencement, duration, and amount. They also require discount rates to convert future expected payments into present values. Some of these assumptions are economic assumptions covered under this ASOP No. 27 and some are non-economic assumptions covered under ASOP No. 35, Selection of Demographic and Other Noneconomic Assumptions for Measuring Pension Obligations. In order to measure a pension obligation, the actuary will need to select or evaluate assumptions underlying the obligation.

3.2 Identification of Economic Assumptions Used in the Measurement

The actuary should consider the following factors when identifying the types of economic assumptions to use for a specific measurement:

a. the purpose of the measurement;

b. the characteristics of the obligation to be measured (measurement period, pattern of plan payments over time, open/closed group, materiality, volatility, etc.); and

c. materiality of the assumption to the measurement (see section 3.5.2).

The types of economic assumptions used to measure obligations under a defined benefit pension plan may include inflation, investment return, discount rate, compensation increases, and other economic factors (for example, Social Security, cost-of-living adjustments, rate of payroll growth, growth of individual account balances, and variable conversion factors).

3.3 General Selection Process

After identifying the economic assumptions to be used for the measurement, the actuary should follow the general process set forth below for selecting each economic assumption for a specific measurement:

a. identify components, if any, of the assumption;

b. evaluate relevant data (section 3.4);

c. consider factors specific to the measurement;

d. consider other general factors (section 3.5); and

e. select a reasonable assumption (section 3.6).

After completing these steps for each economic assumption, the actuary should review the set of economic assumptions for consistency (section 3.12) and make appropriate adjustments if necessary.

3.4 Relevant Data

To evaluate relevant data, the actuary should review appropriate recent and long-term historical economic data. The actuary should not give undue weight to recent experience. The actuary should consider the possibility that some historical economic data may not be appropriate for use in developing assumptions for future periods due to changes in the underlying environment. Appendix 4 lists some generally available sources of economic data and analyses.

3.5 Other General Considerations

The following issues may also be considered when selecting economic assumptions:

3.5.1 Adverse Deviation

Depending on the purpose of the measurement, the actuary may determine that it is appropriate to adjust the economic assumptions to provide for adverse deviation. Any such adjustment made should be disclosed in accordance with section 4.1.1.

3.5.2 Materiality

The actuary should establish a balance between refined economic assumptions and materiality. The actuary is not required to use a type of economic assumption or to select a more refined economic assumption when in the actuary’s professional judgment such use or selection is not expected to produce materially different results.

3.5.3 Cost of Using Refined Assumptions

The actuary should establish a balance between refined economic assumptions and the cost of using refined assumptions. While all material economic assumptions must be reflected, more refined assumptions are not required when they are not expected to produce materially different results. For example, actuaries working with small plans may prefer to emphasize the results of general research to comply with this standard. However, they are not precluded from using relevant plan-specific facts.

3.5.4 Rounding

Taking into account the purpose of the measurement, materiality, and the cost of using refined assumptions, the actuary may determine that it is appropriate to apply a rounding technique to the selected economic assumption. In such cases, the rounding technique should be unbiased.

3.5.5 Changes in Circumstances

The actuary may change the economic assumption that otherwise would have been selected due to an event occurring after the measurement date. For example, a collective bargaining agreement ratified after the measurement date may lead the actuary to change the compensation increase assumption that otherwise would have been selected.

3.5.6 Views of Experts

Economic data and analyses are available from a variety of sources, including representatives of the plan sponsor and administrator, investment advisors, economists, accountants, and other professionals. The actuary may benefit from becoming familiar with a range of views on the factors underlying each chosen assumption. When the actuary is responsible for selecting or giving advice on selecting economic assumptions within the scope of this standard, views of experts may be considered but the selection or advice must reflect the actuary’s professional judgment.

3.6 Selecting a Reasonable Assumption

Each economic assumption selected by the actuary should be reasonable. For this purpose, an assumption is reasonable if it has the following characteristics:

a. It is appropriate for the purpose of the measurement;

b. It reflects the actuary’s professional judgment;

c. It takes into account historical and current economic data that is relevant as of the measurement date;

d. It reflects the actuary’s estimate of future experience, the actuary’s observation of the estimates inherent in financial market data, or a combination thereof; and

e. It is unbiased (i.e., neither optimistic nor pessimistic) – except when provisions for adverse deviation are included and disclosed under section 3.5.1, or when alternative assumptions are used for the assessment of risk.

3.6.1 Reasonable Assumption Based on Future Experience or Market Data

The actuary should develop a reasonable economic assumption based on the actuary’s estimate of future experience, the actuary’s observation of the estimates inherent in financial market data, or a combination thereof. Examples of how the actuary may observe estimates from financial market data include the following:

a. comparing yields on inflation-indexed bonds to yields on equivalent non-inflation-indexed bonds to estimate the market’s expectation of future inflation;

b. comparing yields on bonds of different credit quality to determine market credit spreads;

c. observing yields on U.S. Treasury debt of various maturities to determine a yield curve free of credit risk; and

d. examining annuity prices to estimate the market price to settle pension obligations.

The items listed above, as well as other market observations or prices, include estimates of future experience as well as other considerations. For example, the difference in yields between inflation-linked and non-inflation-linked bonds may include premiums for liquidity and future inflation risk in addition to an estimate of future inflation. The actuary may want to adjust estimates based on observations to reflect the various risk premiums included in market pricing.

3.6.2 Range of Reasonable Assumptions

The actuary should recognize the uncertain nature of the items for which assumptions are selected and, as a result, may consider several different assumptions equally reasonable for a given measurement. The actuary should also recognize that different actuaries will apply different professional judgment and may choose different reasonable assumptions. As a result, a range of reasonable assumptions may develop across actuarial practice.

3.7 Selecting an Inflation Assumption

If the actuary is using an approach that treats inflation as an explicit component of other economic assumptions or as an independent assumption, the actuary should follow the general process set forth in section 3.3 to select an inflation assumption.

3.7.1 Data

The actuary should review appropriate inflation data. These data may include consumer price indices, the implicit price deflator, forecasts of inflation, yields on government securities of various maturities, and yields on nominal and inflation-indexed debt.

3.7.2 Select and Ultimate Inflation Rates

The actuary may assume select and ultimate inflation rates in lieu of a single inflation rate. Select and ultimate inflation rates vary by period from the measurement date (for example, inflation of 3% for the first 5 years following the measurement date and 4% thereafter).

3.8 Selecting an Investment Return Assumption

The investment return assumption reflects the anticipated returns on the plan’s current and, if appropriate for the measurement, future assets. This assumption is typically constructed by considering various factors including, but not limited to, the time value of money; inflation and inflation risk; illiquidity; credit risk; macroeconomic conditions; and growth in earnings, dividends, and rents.

In developing a reasonable assumption for these factors and in combining the factors to develop the investment return assumption, the actuary may consider a broad range of data and other inputs, including the judgment of investment professionals.

3.8.1 Data

The actuary should review appropriate investment data. These data may include the following:

a. current yields to maturity of fixed income securities such as government securities and corporate bonds;

b. forecasts of inflation, GDP growth, and total returns for each asset class;

c. historical and current investment data including, but not limited to, real and nominal returns, the inflation and inflation risk components implicit in the yield of inflation-protected securities, dividend yields, earnings yields, and real estate capitalization rates; and

d. historical plan performance.

The actuary may also consider historical and current statistical data showing standard deviations, correlations, and other statistical measures related to historical or future expected returns of each asset class and to inflation. Stochastic simulation models may be used to develop expected investment returns from this statistical data.

3.8.2 Components of the Investment Return Assumption

The investment return assumption can be developed using various methods consistent with the principles set forth in this standard, including combining estimated components of the assumption. Where the assumption is determined as the result of a combination of two or more components or factors, care should be taken to ensure that the combination of these factors is logically consistent.

3.8.3 Measurement-Specific Considerations

The following factors should be considered in developing an investment return assumption:

a. Investment Policy—The plan’s investment policy may include the following: (i) the current allocation of the plan’s assets; (ii) types of securities eligible to be held (diversification, marketability, social investing philosophy, etc.); (iii) a target allocation of plan assets among different classes of securities; and (iv) permissible ranges for each asset class within which the investment manager is authorized to make investment decisions. The actuary should consider whether the current investment policy is expected to change during the measurement period.

b. Effect of Reinvestment—Two reinvestment risks are associated with traditional, fixed income securities: (i) reinvestment of interest and normal maturity values not immediately required to pay plan benefits, and (ii) reinvestment of the entire proceeds of a security that has been called by the issuer.

c. Investment Volatility—Plans investing heavily in those asset classes characterized by high variability of returns may be required to liquidate those assets at depressed values to meet benefit obligations. Other investment risks may also be present, such as default risk or the risk of bankruptcy of the issuer.

d. Investment Manager Performance—Anticipating superior (or inferior) investment manager performance may be unduly optimistic (or pessimistic). The actuary should not assume that superior or inferior returns will be achieved, net of investment expenses, from an active investment management strategy compared to a passive investment management strategy unless the actuary has reason to believe, based on relevant supporting data, that such superior or inferior returns represent a reasonable expectation over the measurement period.

e. Investment and Other Administrative Expenses—Investment and other administrative expenses may be paid from plan assets. To the extent such expenses are not otherwise recognized, the actuary should reduce the investment return assumption to reflect these expenses.

f. Cash Flow Timing—The timing of expected contributions and benefit payments may affect the plan’s liquidity needs and investment opportunities.

g. Benefit Volatility—Benefit volatility may be a primary factor for small plans with unpredictable benefit payment patterns. It may also be an important factor for a plan of any size that provides highly subsidized early retirement benefits, lump-sum benefits, or supplemental benefits triggered by corporate restructuring or financial distress. In such plans, the untimely liquidation of securities at depressed values may be required to meet benefit obligations.

h. Expected Plan Termination—In some situations, the actuary may expect the plan to be terminated at a determinable date. For example, the actuary may expect a plan to terminate when the owner retires, or a frozen plan to terminate when assets are sufficient to provide all accumulated plan benefits. In these situations, the investment return assumption may reflect a shortened measurement period that ends at the expected termination date.

i. Tax Status of the Funding Vehicle—If the plan’s assets are not kept in a tax-exempt fund, income taxes may reduce the plan’s investment return. Taxes may be reflected by an explicit reduction in the total investment return assumption or by a separately identified assumption.

j. Arithmetic and Geometric Returns—The use of a forward looking expected arithmetic return as an investment return assumption will produce a mean accumulated value. The use of a forward looking expected geometric return as an investment return assumption will produce an accumulated value that generally converges to the median accumulated value as the time horizon lengthens. The actuary should consider the implications of a forward looking expected arithmetic return and a forward looking expected geometric return when constructing an investment return assumption.

In some instances, the actuary will receive forward looking expected returns by asset class from an investment professional. The actuary should ensure that the type of forward looking expected returns received from the investment professional is known (i.e., forward looking expected geometric returns or forward looking expected arithmetic returns) and that the forward looking expected returns are used appropriately. For example, when determining a forward looking expected geometric return for an entire portfolio, the actuary generally should not take the weighted average of the forward looking expected geometric return for each of the asset classes. In this instance, to determine the forward looking expected geometric return for an entire portfolio, the actuary should take the weighted average of the forward looking expected arithmetic return for each of the asset classes and adjust such determination to reflect the variance of the entire portfolio.

Appendix 3 includes general background on arithmetic and geometric returns

3.8.4 Multiple Investment Return Rates

The actuary may assume multiple investment return rates in lieu of a single investment return rate. Two examples are as follows:

a. Select and Ultimate Investment Return Rates—Assumed investment return rates vary by period from the measurement date (for example, returns of 8% for the first 10 years following the measurement date and 6% thereafter). When assuming select and ultimate investment return rates, the actuary should consider the relationships among inflation, interest rates, and market appreciation (depreciation).

b. Benefit Payments Covered by Designated Current Assets—One investment return rate is assumed for benefit payments covered by designated current plan assets on the measurement date, and a different investment return rate is assumed for the balance of the benefit payments and assets.

3.9 Selecting a Discount Rate

The discount rate is used to measure the present value of expected future plan payments. The discount rate may be a single rate or a series of rates, such as a yield curve. The actuary should consider the purpose of the measurement as a primary factor in selecting a discount rate. Some examples of measurement purposes are as follows:

a. Contribution Budgeting—An actuary evaluating the sufficiency of a plan’s contribution policy may choose among several discount rates. The actuary may use a discount rate that reflects the anticipated investment return from the pension fund. Alternatively, the actuary may use discount rates appropriate for defeasance, settlement or market measurements.

b. Defeasance or Settlement—An actuary measuring a plan’s present value of benefits on a defeasance or settlement basis may use a discount rate equal to rates implicit in annuity prices or other settlement options.

c. Market Measurements—An actuary making a market measurement may use a set of discount rates based on market yields for a hypothetical bond portfolio whose cash flows reasonably match the pattern of benefits that are expected to be paid in the future. The type and quality of bonds in the hypothetical portfolio may depend on the particular type of market measurement.

d. Pricing—An actuary measuring the price of plan amendments may use a discount rate implicit in the prices for obligations with similar characteristics in financial markets. An actuary who wants to determine a plan sponsor’s future contributions that are expected to support the plan amendment may use rates described in section 3.9(a).

The present value of expected future pension payments may be calculated from the perspective of different parties, recognizing that different parties may have different measurement purposes. For example, the present value of expected future payments could be calculated from the perspective of an outside creditor or the entity responsible for funding the plan. The outside entity may desire a discount rate consistent with other measurements of importance to the creditor even though those other measurements may have little or no importance to the entity funding the plan.

3.10 Selecting a Compensation Increase Assumption

Compensation is a factor in determining participants’ benefits in many pension plans. Also, some actuarial cost methods take into account the present value of future compensation. Generally, a participant’s compensation will increase over the long term in accordance with inflation, productivity growth, and merit adjustments. The assumption used to measure the anticipated year-to-year change in compensation is referred to as the compensation increase assumption. It may be a single rate, it may vary by age or service, or it may vary over future years. The actuary should consider the following factors when selecting a compensation increase assumption.

3.10.1 Data

The actuary should review available compensation data. These data may include the following:

a. the plan sponsor’s current compensation practice and any anticipated changes in this practice;

b. current compensation distributions by age or service;

c. historical compensation increases and practices of the plan sponsor and other plan sponsors in the same industry or geographic area; and,

d. historical national wage increases and productivity growth.

The actuary should consider available plan-sponsor-specific compensation data, but the actuary must carefully weigh the credibility of these data when selecting the compensation increase assumption. For small plans or recently formed plan sponsors, industry or national data may provide a more appropriate basis for developing the compensation increase assumption.

3.10.2 Measurement-Specific Considerations

The actuary should consider factors specific to each measurement in selecting a specific compensation increase assumption. Examples of such factors are as follows:

a. Compensation Practice—The plan sponsor’s current compensation practice and any contemplated changes may affect the compensation increase assumption, at least in the short term. For example, if pension benefits are a function of base compensation and the plan sponsor is changing its compensation practice to put greater emphasis on incentive compensation, future growth in base compensation may differ from historical patterns.

b. Competitive Factors—The level and pattern of future compensation changes may be affected by competitive factors, including competition for employees both within the plan sponsor’s industry and within the geographical areas in which the plan sponsor operates, and global price competition. Unless the measurement period is short, the actuary should not give undue weight to short-term patterns.

c. Collective Bargaining—The collective bargaining process impacts the level and pattern of compensation changes. However, it may not be appropriate to assume that future contracts will provide the same level of compensation changes as the current or recent contracts. For example, if the current contract provides for a compensation freeze, it would generally be inappropriate to assume that such a policy would continue indefinitely after the contract expires.

d. Compensation Volatility—If certain elements of compensation, such as bonuses and overtime, tend to vary materially from year to year, or if aberrations exist in recent compensation amounts, then volatility should be taken into account. In some circumstances, this may be accomplished by adjusting the base amount from which future compensation elements are projected (for example, the projected bonuses might be based on an adjusted average of bonuses over the last 3 years). In some other circumstances, an additional assumption regarding an expected increase in pay in the final year of service may be used.

e. Expected Plan Freeze or Termination—In some situations, as stated in section 3.8.3(h), the actuary may expect the plan to be frozen or terminated at a determinable date. In these situations, the compensation increase assumption may reflect a shortened measurement period that ends at the expected termination date.

3.10.3 Multiple Compensation Increase Assumptions

The actuary may use multiple compensation increase assumptions in lieu of a single compensation increase assumption. Three examples are as follows:

a. Select and Ultimate Assumptions—Assumed compensation increases vary by period from the measurement date (for example, 4% increases for the first 5 years following the measurement date, and 5% thereafter) or by age or service.

b. Separate Assumptions for Different Employee Groups—Different compensation increases are assumed for two or more employee groups that are expected to receive different levels or patterns of compensation increases.

c. Separate Assumptions for Different Compensation Elements—Different compensation increases are assumed for two or more compensation elements that are expected to change at different rates (for example, 5% bonus increases and 3% increases in other compensation elements).

3.11 Selecting Other Economic Assumptions

In addition to inflation, investment return, discount rate, and compensation increase assumptions, the following are some of the types of economic assumptions that may be required for measuring certain pension obligations. The actuary should follow the general process described in section 3.3 to select these assumptions. The selected assumptions should also satisfy the consistency requirement of section 3.12.

Social Security benefits are based on an individual’s covered earnings, the OASDI contribution and benefit base, and changes in the cost of living. Changes in the OASDI contribution and benefit base are determined from changes in national average wages, which reflect the change in national productivity and inflation.

3.11.2 Cost-of-Living Adjustments

Plan benefits or limits affecting plan benefits (including the Internal Revenue Code section 401(a)(17) compensation limit and section 415(b) maximum annuity) may be automatically adjusted for inflation or assumed to be adjusted for inflation in some manner (for example, through regular plan amendments). However, for some purposes (such as qualified pension plan funding valuations), the actuary may be precluded by applicable laws or regulations from anticipating future plan amendments or future cost-of-living adjustments in certain IRC limits.

3.11.3 Rate of Payroll Growth

As a result of terminations and new participants, total payroll generally grows at a different rate than does a participant’s salary or the average of all current participants combined. As such, when a payroll growth assumption is needed, the actuary should use an assumption that is consistent with but typically not identical to the compensation increase assumption. One approach to setting the payroll growth assumption may be to reduce the compensation increase assumption by the effect of any assumed merit increases. The actuary should apply professional judgment in determining whether, given the purpose of the measurement, the payroll growth assumption should be based on a closed or open group and, if the latter, whether the size of that group should be expected to increase, decrease, or remain constant.

3.11.4 Growth of Individual Account Balances

Certain plan benefits have components directly related to the accumulation of real or hypothetical individual account balances (for example, so-called floor-offset arrangements and cash balance plans). Further guidance regarding these types of benefits is included in ASOP No. 4.

3.11.5 Variable Conversion Factors

Measuring certain pension plan obligations may require converting from one payment form to another, such as converting a projected individual account balance to an annuity, converting an annuity to a lump sum, or converting from one annuity form to a different annuity form. The conversion factors may be variable (for example, recalculated each year based on a stated mortality table and interest rate equal to the yield on 30-year Treasury bonds).

3.12 Consistency among Economic Assumptions Selected by the Actuary

With respect to any particular measurement, each economic assumption selected by the actuary should be consistent with every other economic assumption selected by the actuary for the measurement period, unless the assumption, considered individually, is not material, as provided in section 3.5.2. A number of factors may interact with one another and may be components of other economic assumptions, such as inflation, economic growth, and risk premiums. In some circumstances, consistency may be achieved by using the same inflation, economic growth and other relevant components in each of the economic assumptions selected by the actuary.

Consistency is not necessarily achieved by maintaining a constant difference between one economic assumption and another. For each measurement date, the actuary should reevaluate both the individual assumptions and the relationships among them, and make appropriate adjustments.

Assumptions selected by the actuary need not be consistent with prescribed assumptions, which are discussed in section 3.13.

3.13 Prescribed Assumption(s)

The actuary should use the principles set forth in this standard whenever the actuary has an obligation to assess the reasonableness of a prescribed assumption. The actuary’s obligations with respect to prescribed assumptions are governed by ASOP Nos. 4, 6, or 41 as applicable, which address prescribed assumptions and methods.

3.14 Changing Assumptions

An actuary’s assumption with respect to a particular measurement of pension obligations may change from time to time due to changing conditions or emerging plan experience. Even if assumptions are not changed, the actuary should be satisfied that each of the economic assumptions selected for a particular measurement complies with this standard.

Section 4. Communications and Disclosures

4.1 Communications

Pension actuarial communications should contain the following disclosures:

4.1.1 Economic Assumptions

The actuary should describe each economic assumption used in the measurement, including whether the assumption represents an estimate of future experience, the actuary’s observation of the estimates inherent in financial market data, or a combination thereof. Sufficient detail should be shown to assess the level and pattern of each assumption.

Depending on a particular measurement’s circumstances, the actuary may give information about specific interrelationships among the assumptions (for example, investment return: 8% per year, net of investment expenses and including inflation at 3%). The description should also include a disclosure of any adjustment for adverse deviation made in accordance with section 3.5.1.

4.1.2 Rationale for Assumptions

The actuary should disclose the information and analysis used in selecting each non-prescribed economic assumption that has a significant effect on the measurement. The disclosure may be brief but should be pertinent to the plan’s circumstances. For example, the actuary may disclose any specific approaches used, sources of external advice, and how past experience and future expectations were considered. The disclosure may reference any actuarial experience report or study performed, including the date of the report or study.

4.1.3 Changes in Assumptions

The actuary should disclose any changes in the non-prescribed economic assumptions from those previously used for the same type of measurement. For assumptions that were not prescribed, the actuary should include an explanation of the information and analysis that led to those changes. The general effects of the changes should be disclosed in words or by numerical data, as appropriate. The disclosure may be brief but should be pertinent to the plan’s circumstances. The disclosure may reference any actuarial experience report or study performed, including the date of the report or study.

4.1.4 Changes in Circumstances

The actuary should refer to ASOP No. 41 for communication and disclosure requirements regarding changes in circumstances known to the actuary that occur after the measurement date and that would affect economic assumptions selected as of the measurement date.

4.2 Additional Disclosures

The actuary should include the following, as applicable, in an actuarial communication:

a. the disclosure in ASOP No. 41, section 4.2, for any material prescribed assumption or method set by law, as defined in section 2.6;

b. the disclosure in ASOP No. 41, section 4.3 for any material prescribed assumption or method set by another party, as defined in section 2.5;

c. the disclosure in ASOP No. 41, section 4.3, if the actuary states reliance on other sources and thereby disclaims responsibility for any material assumption or method selected by a party other than the actuary; and

d. the disclosure in ASOP No. 41, section 4.4, if, in the actuary’s professional judgment, the actuary has otherwise deviated materially from the guidance of this ASOP.

Appendix 1 – Background and Current Practices

Note: This appendix is provided for informational purposes, but is not part of the standard of practice.

Background

Economic assumptions have a significant effect on any pension obligation measurement. Small changes of 25 or 50 basis points in these assumptions can change the measurement by several percentage points or more. Assumptions such as compensation increases or cash balance crediting rates are often used to determine projected benefit streams for valuation purposes. The discount rate assumption, arguably the most critical economic assumption in determining a pension obligation, is used to determine the discounted present value of all benefit streams that are part of such obligation measurement.

Historically, actuaries have used various practices for selecting economic assumptions. For example, some actuaries have looked to surveys of economic assumptions used by other actuaries, some have relied on detailed research by experts, some have used highly sophisticated projection techniques, and many actuaries have used a combination of these.

The first decade of the 21st Century contained a significant amount of debate inside and outside the actuarial profession regarding the measurement of pension obligations. Much of the debate centered on the economic assumptions actuaries use to measure these obligations. The decade also saw the emergence of a financial economic viewpoint on pension obligations. Applying financial economic theory to the measurement of pension obligations has been controversial and has produced a significant amount of debate in the actuarial profession.

Current Practices

The actuary’s discretion over economic assumptions has been curtailed in many situations. In the private single employer plan arena, the IRS, PBGC, and FASB have promulgated rulings that have limited or effectively removed an actuary’s judgment regarding the discount rate used for current year funding or accounting. Actuaries can still set other economic assumptions, such as compensation increases, inflation, or fixed income yields.

For plans other than private single employer plans (for example, church plans, multiemployer plans, public plans), the discount rate for current year funding requirements may or may not be prescribed by other entities. Funding valuations for these types of plans often use a discount rate related to the expected return on plan assets. In practice, this discount rate (return on asset) assumption may be set by the legislative body, plan sponsor, a governing board of trustees, or the actuary. The actuary may advise the plan sponsor about the selection of the discount rate.

As in the single-employer situation, the actuary may have discretion over other economic assumptions used to measure obligations for plans other than private single-employer plans. Alternatively, the actuary may be in an advisory position, helping the legislative body, plan sponsor, or governing board of trustees select the assumptions.

The focus on solvency in the private single employer plan arena has come along with prescribed economic assumptions that are linked to capital market indices. Actuaries practicing in this area are becoming accustomed to changing assumptions frequently. In non-prescribed situations, practice is still dependent upon the individual actuary. Many actuaries change assumptions infrequently, while other actuaries reevaluate the assumptions as of each measurement date and change economic assumptions more frequently. In the public plan arena, many entities perform assumption reviews every few years and the reviews may or may not lead to assumption adjustments.

In preparing calculations for purposes other than current year plan valuations, actuaries often use economic assumptions that are different from those used for the current year valuation.

Appendix 2 – Comments on the First Exposure Draft and Responses

The first exposure draft of this proposed revision of this ASOP, Selection of Economic Assumptions for Measuring Pension Obligations, was issued in January 2011 with a comment deadline of April 30, 2011. Twenty comment letters were received, some of which were submitted on behalf of multiple commentators, such as by firms or committees. For purposes of this appendix, the term “commentator” may refer to more than one person associated with a particular comment letter. The Pension Committee carefully considered all comments received, and the ASB reviewed (and modified, where appropriate) the proposed changes.

Click here to view Appendix 2 in its entirety.

Appendix 3 – Arithmetic and Geometric Returns

A. Introduction

One of the most important assumptions an actuary uses in measuring pension obligations is the discount rate. As part of the Exposure Draft of ASOP No. 27 issued in January 2011, the following question was included in the Transmittal Memorandum:

“4. Do you agree that the guidance on arithmetic and geometric returns is appropriate? Should the consequences of the use of geometric or arithmetic returns be disclosed?”

Given the wide range of responses received to the above question, the Pension Committee of the Actuarial Standards Board determined that the inclusion of some educational material regarding arithmetic and geometric returns in ASOP No. 27 would be beneficial. The following material is not meant to be an exhaustive discussion of the matter. It is meant to give the actuary some direction as to the considerations that may be employed in determining whether the use of arithmetic or geometric returns is more appropriate in the selection of a discount rate. In many circumstances, as with the selection of other assumptions, the purpose of the measurement is one of the most important determinants.

The use of a forward looking expected geometric return as a discount rate will produce a present value that generally converges to the median present value as the time horizon lengthens (i.e., if the actuary determines a funding obligation using the forward looking expected geometric return to discount the obligation to produce a present value, it is expected that in the limiting case there will be enough money to fund the obligation 50% of the time.) The use of a forward looking expected arithmetic return as a discount rate will generally produce a mean present value (i.e., there will be no expected actuarial gains and/or losses).

This appendix should not be construed as endorsing plan asset based present value measurements (i.e., traditional actuarial measurements) over non-plan asset based present value measurements (i.e., market consistent measurements).

B. Looking Back Versus Looking Forward

The discount rate used in the measurement of a pension obligation is a forward-looking assumption. For a plan asset based present value measurement, while the actuary may use some historical results in establishing expectations regarding the future, the discount rate is an expectation of events to come, not events that have already occurred. For a non-plan asset based present value calculation, the discount rate is a version of a yield curve as of the measurement date, not of a version of a yield curve that existed in the past.

One of the more confusing aspects of the debate regarding arithmetic and geometric returns is

a. determining if we are talking about using historical results to establish forward looking (i.e., future) expectations, or

b. determining if we are talking about whether a forward looking expected geometric return or forward looking expected arithmetic return is a more appropriate discount rate.

Note that a forward looking expected geometric return is not synonymous with compounding. That is, both a forward looking expected geometric return and a forward looking expected arithmetic return would be used in a compounding nature.

C. An Example

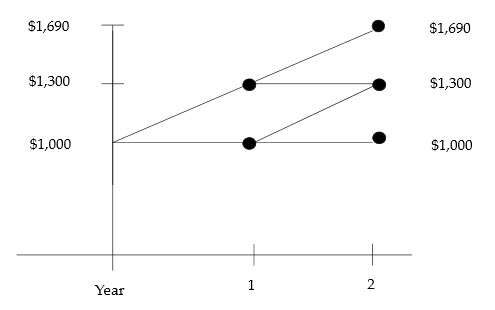

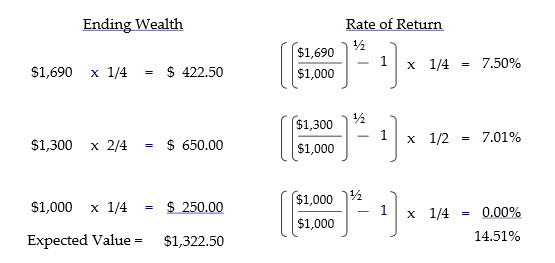

The following example illustrates the use of a forward looking expected arithmetic return to produce a mean present value. Assume that an asset class is expected to have a 50% probability of earning a return of 30% and a 50% probability of earning a return of 0% for each of the next two years and that these returns are the only possible outcomes. (The forward looking expected arithmetic return in this example would be 15%.) The chart below illustrates the totality of possible investment results for an initial $1,000 investment placed in this asset class:

The expected ending wealth values and a derivation of the forward looking expected geometric return is presented below:

The forward looking expected geometric return in this example is 14.51%. The question then becomes what discount rate would take the expected value of $1,322.50 at the end of year 2 and produce a present value of $1,000? The answer is shown below:

which is the forward looking expected arithmetic return. Note however in this simple example, that if the actuary funded an obligation that is expected to be $1,322.50 at the end of year two with a one-time payment of $1,000 at the beginning of year 0, there would be insufficient funds at the end of year 2 three-quarters of the time.

D. Capital Market Assumptions from Investment Consultants

In many instances, the actuary will receive capital market assumptions from an investment consultant that the actuary will then use to determine the forward looking expected arithmetic return and/or the forward looking expected geometric return. The capital market assumptions can be broadly classified into the following categories:

a. expected returns by asset class;

b. standard deviations by asset class; and

c. correlation coefficients between asset classes.

With respect to expected returns by asset class, some investment consultants will provide forward looking expected arithmetic returns, some will provide forward looking expected geometric returns and some will provide both. It is important to understand what was received from the investment consultant as well as the future time horizon to which the expectations apply.

In general, a forward looking expected geometric return for an asset class can be approximated by taking the forward looking expected arithmetic return and subtracting one-half of the variance of the asset class¹.

If the actuary is trying to determine the forward looking expected arithmetic return for an entire portfolio from individual asset classes, this can be accomplished by taking the appropriate weightings from the individual asset classes’ forward looking expected arithmetic returns. However, if the actuary is trying to determine the forward looking expected geometric return for an entire portfolio from individual asset classes, this cannot be accomplished by taking the appropriate weightings from the individual asset classes’ forward looking expected geometric returns. In approximating the forward looking expected geometric return for the entire portfolio, the actuary would first determine the forward looking expected arithmetic return for the entire portfolio and then subtract one-half of the variance of the entire portfolio.

Appendix 4 – Selected References for Economic Data and Analyses

The following list of references is a representative sample of available sources. It is not intended to be an exhaustive list.

- General Comprehensive Sources

a. Kellison, Stephen G. The Theory of Interest. 3rd ed. Colorado Springs, CO: McGraw-Hill, 2008.

b. Statistics for Employee Benefits Actuaries. Committee on Retirement Systems Practice Education, and the Pension and Health Sections, Society of Actuaries. Updated annually.

c. Stocks, Bonds, Bills, and Inflation (SBBI). Chicago, IL: Ibbotson Associates. Annual Yearbook, market results 1926 through previous year.

- Recent Data, Various Indexes, and Some Historical Data

a. Barron’s National Business and Financial Weekly. Dow Jones and Co., Inc. Available on newsstands and by subscription.

b. U.S. Bureau of the Census. Statistical Abstract of the United States. Published annually.

c. U.S. Department of Labor, Bureau of Labor Statistics. Consumer Price Index. Monthly updates of CPI-U and CPI-W by expenditure category and commodity and service group. Available by subscription from the U.S. Government Printing Office, Washington, DC 20402.

d. U.S. Federal Reserve Monthly Statistical Release G.13. Interest rate information for selected Treasury securities. Federal Reserve Board, Publications Services, Washington, DC 20551. Available by subscription.

e. U.S. Federal Reserve Weekly Statistical Release H.15. Interest rate information for selected Treasury securities. Available as above.

f. U.S. House of Representatives, Committee on Ways and Means. Green Book: Background Material and Data on Programs within the Jurisdiction of the Committee. Washington, DC: Government Printing Office. Published annually.

g. U.S. Social Security Administration. Social Security Bulletin. Annual Statistical Supplements, Trustee Reports, and quarterly Bulletin. Available by subscription from the U.S. Government Printing Office, Washington, DC 20402.

h. The Wall Street Journal. Daily periodical. Money and Investing (section 3); and stocks (6 indexes), bonds (4 indexes), and interest (4 indexes). Available on newsstands and by subscription.

- Forecasts

a. Blue Chip Financial Forecasts. Published by Capital Publications, Inc., P.O. Box 1453, Alexandria, VA 22313-2053. March and October issues contain long-range forecasts for interest rates and inflation.

b. Congressional Budget Office’s 5-year economic forecast. The forecast projects three-month Treasury Bill rates, 10-year Treasury Note rates, CPI-U, gross domestic product, and unemployment rates. Prepared annually. Washington, DC: Government Printing Office.

1. Investments, Bodie, Kane and Marcus, 2005, p. 864.

PDF Version: Download Here

Last Revised: January 2012

Document Status: Past Exposure Draft