ACTUARIAL STANDARD OF PRACTICE NO. 3

Continuing Care Retirement Communities

and At Home Programs

STANDARD OF PRACTICE

TRANSMITTAL MEMORANDUM

TO: Members of Actuarial Organizations Governed by the Standards of Practice of the Actuarial Standards Board and Other Persons Interested in Continuing Care Retirement Communities and At Home Programs

FROM: Actuarial Standards Board (ASB)

SUBJ: Actuarial Standard of Practice (ASOP) No. 3

This document contains the revision of ASOP No. 3, Continuing Care Retirement Communities and At Home Programs.

History of the Standard

In 1987, the Interim Actuarial Standards Board adopted a document titled Relating to Continuing Care Retirement Communities (CCRCs). In 1990, the ASB revised and reformatted ASOP No. 3, Relating to Continuing Care Retirement Communities. In 1994, the ASB adopted another revision titled Practices Relating to Continuing Care Retirement Communities. In 2008, the standard was revised to reflect current, generally accepted actuarial practice and to adopt the updated format for standards. The industry also refers to Continuing Care Retirement Communities (CCRCs) as Life Plan Communities (LPCs), and for the purpose of this standard CCRCs refers to both CCRCs and LPCs.

Within CCRCs, the provision of benefits through At Home Programs has emerged as a new area of practice. Various terms are used in the industry to describe At Home Programs, which are most commonly known as Continuing Care At Home and Lifecare At Home Programs. This ASOP addresses actuarial practice for both CCRCs and At Home Programs. For the purposes of this ASOP, the term “CCRC” reflects the traditional industry product and the term “At Home Program” reflects benefits offered to members who are not residents.

CCRCs arose from a desire of individuals to have both housing and long-term care provided by the same organization. Over time, the CCRC model has evolved, with contracts providing for individuals who have delayed entry to a CCRC as well as individuals who may have never intended to move into a CCRC. At Home Programs cover members who do not intend to move into the CCRC. Many states have developed regulations to address both traditional CCRCs and At Home Programs under the CCRC umbrella. Several states limit At Home Programs to the confines of an existing CCRC.

Exposure Draft

The exposure draft was issued in November 2020 with a comment deadline of February 1, 2021. Five comment letters were received and considered in making changes that are reflected in the final ASOP.

Notable Changes from Exposure Draft

Notable changes made to the exposure draft are summarized below. Notable changes do not include changes made to improve readability, clarity, or consistency.

- The terms “resident” and “non-resident” were replaced with “contractual resident” and “non-contractual resident” throughout the ASOP.

- Examples of services covered by the ASOP proposed to be deleted in the exposure draft were restored in section 1.2, Scope.

- A definition for “occupancy rate” was added in section 2.20, and the occupancy rate assumption was included in section 3.7.1, Actuarial Assumptions.

- Guidance was clarified regarding the consistency among related assumptions in section 3.7.6, Reasonableness of Assumptions.

- Guidance was clarified to state that the combined effect of financial and demographic assumptions is expected to have no significant bias except for margins for uncertainty in section 3.7.6, Reasonableness of Assumptions.

Notable Changes from the Existing ASOP

A cumulative summary of the notable changes from the existing ASOP is summarized below. Notable changes do not include additional changes made to improve readability, clarity, or consistency.

- The ASOP was revised to address actuarial practice for At Home Programs that are not regulated as an insurance entity.

- The ASOP was revised to include new disclosure requirements that the ASB believes are appropriate and are intended to enhance the quality of actuarial communications regarding CCRCs and At Home Programs.

The ASB thanks everyone who took the time to contribute comments and suggestions on the exposure draft.

The ASB would like to posthumously thank Matthew P. Chamblee for his contribution to the ASB Health Committee.

The ASB voted in September 2021 to adopt this standard.

| ASOP No. 3 Task Force | ||

| Dave Bond, Chairperson | ||

| Christopher J. Borcik | Molly J. Shaw | |

| John C. Lloyd | Darryl G. Wagner | |

| Lisa M. Parker | Gregory T. Zebolsky | |

| Health Committee of the ASB | ||

| Rick Lassow, Chairperson | ||

| Jinn-Feng Lin | Jennifer L. Stevenson | |

| Daniel S. Pribe | Alisa L. Swann | |

| D. Todd Sherman | Timothy J. Wilder | |

| David T. Stefanski | ||

| Actuarial Standards Board | ||

| Darrell D. Knapp, Chairperson | ||

| Elizabeth K. Brill | Cande J. Olsen | |

| Robert M. Damler | Kathleen A. Riley | |

| Kevin M. Dyke | Judy K. Stromback | |

| David E. Neve | Patrick B. Woods | |

The Actuarial Standards Board (ASB) sets standards for appropriate actuarial practice in the United States through the development and promulgation of Actuarial Standards of Practice (ASOPs). These ASOPs describe the procedures an actuary should follow when performing actuarial services and identify what the actuary should disclose when communicating the results of those services.

ACTUARIAL STANDARD OF PRACTICE NO. 3

CONTINUING CARE RETIREMENT COMMUNITIES AND AT HOME PROGRAMS

STANDARD OF PRACTICE

Section 1. Purpose, Scope, Cross References, and Effective Date

1.1 Purpose

This actuarial standard of practice (ASOP or standard) provides guidance to actuaries when performing actuarial services with respect to Continuing Care Retirement Communities (CCRCs), also known as Life Plan Communities (LPCs), or At Home Programs that are not regulated as insurance entities.

1.2 Scope

This standard applies to actuaries when performing actuarial services, including giving advice, in connection with CCRCs (including nonprofit and for-profit entities) or At Home Programs that are not regulated as insurance entities. These actuarial services may be performed for owners, operators, financing entities, or current or prospective contractual residents or members, as well as for other professionals or regulatory bodies.

Examples of the services covered by this ASOP include the following:

- testing the financial condition for satisfactory actuarial balance;

- estimating actuarial values of assets and liabilities;

- evaluating the fee structure for existing contractual residents or members, or a cohort of new contractual residents or members;

- developing population projections, including contractual resident or member movements, independent living unit turnover, and health center utilization;

- projecting future cash flows and cash and investment balances;

- designing and pricing new residency agreements or membership agreements;

- estimating the future services obligation under GAAP;

- assisting in developing financial feasibility studies;

- performing mortality, morbidity, and withdrawal experience studies; and

- providing appropriate rates of mortality, morbidity, or life expectancies.

This standard does not apply to actuaries when performing actuarial services with respect to At Home Programs regulated as insurance entities. When performing actuarial services with respect to such organizations, the actuary should review ASOP No. 18, Long-Term Care Insurance, for applicability.

If the actuary determines that the guidance in this ASOP conflicts with a cross-practice ASOP (applies to all practice areas), this ASOP governs.

If the actuary departs from the guidance set forth in this standard in order to comply with applicable law (statutes, regulations, and other legally binding authority), or for any other reason the actuary deems appropriate, the actuary should refer to section 4. If a conflict exists between this standard and applicable law, the actuary should comply with applicable law.

1.3 Cross References

When this standard refers to the provisions of other documents, the reference includes the referenced documents as they may be amended or restated in the future, and any successor to them, by whatever name called. If any amended or restated document differs materially from the originally referenced document, the actuary should consider the guidance in this standard to the extent it is applicable and appropriate.

1.4 Effective Date

This standard is effective for work performed on or after June 1, 2022.

Section 2. Definitions

The terms below are defined for use in this actuarial standard of practice and appear in bold throughout the ASOP.

2.1 Actuarial Balance Sheet

A measure of the assets and liabilities, as of the valuation date, associated with current contractual residents or current members.

2.2 Actuarial Present Value

The value of an amount or series of amounts payable or receivable at various times, determined as of a given date by the application of a particular set of actuarial assumptions with regard to future events, observations of market or other valuation data, or a combination of assumptions and observations.

2.3 Additional Fee

An amount that may be payable by a contractual resident or member, in accordance with a residency agreement or membership agreement, for services made available but not covered by the advance fee and the periodic fees. Examples of additional fees include fees for guest meals, additional meals, barber/beauty shop, use of a carport, and non-covered health care services.

2.4 Advance Fee

An amount payable by a contractual resident at the inception of a residency agreement or by a member at the inception of a membership agreement. The advance fee is usually specified in the residency agreement or membership agreement and is usually payable prior to occupancy of the residence or receipt of benefits.

2.5 At Home Program

An organization that provides social and health care services in return for some combination of an advance fee, periodic fees, and additional fees. At Home Programs differ from CCRCs in that they do not provide a direct independent living unit for members.

2.6 Cash and Investment Balance

The value of cash, cash equivalents, and marketable securities (historically referred to as “cash balance” by industry organizations). This excludes the value of the physical property assets.

2.7 Cohort of New Contractual Residents or New Members

A hypothetical group of new contractual residents or members assumed to enter a CCRC or At Home Program over a specified period of time and assumed to have certain demographic characteristics.

2.8 Continuing Care Retirement Community (CCRC)

An organization that provides contractual residential housing and stated housekeeping, social, and health care services in return for some combination of an advance fee, periodic fees, and additional fees. CCRCs are also known as Life Plan Communities (LPCs).

2.9 Contractual Resident

A person who has signed a residency agreement.

2.10 Fee Structure

A combination of fees that includes advance fees and periodic fees, and that may include additional fees.

2.11 Health Care Guarantee

A clause in a residency agreement or membership agreement guaranteeing access to health care and defining the type of health care services to be provided to the contractual resident or member. These health care services may be offered with or without adjustments to the periodic fees.

2.12 Health Center

A facility associated with a CCRC or At Home Program where health care is provided to contractual residents or members in accordance with the residency agreement or membership agreement. The facility typically includes some combination of assisted living, memory care, and nursing care units. Non-contractual residents may also live in the facility.

2.13 Independent Living Unit

Living quarters designed for contractual residents capable of living independently. A contractual resident could receive home health care in the independent living unit, but a contractual resident who needs full-time health care on either a temporary or permanent basis is normally transferred to the health center.

2.14 Level(s) of Care

Varying degrees of care based on a contractual resident’s or member’s health status. Typical levels of care include independent living, assisted living, nursing care, and memory care. The levels of care may be dictated by state licensure.

2.15 Living Unit

The various living quarters of a CCRC, including independent living units and health center units.

2.16 Member

A person who has signed a membership agreement with an At Home Program.

2.17 Membership Agreement

A contract between one or more members and an At Home Program that describes the services to be provided, the obligations of the parties, the health care guarantee, and any refund guarantee. The contract is usually of long duration and may be for the life of each member.

2.18 Morbidity

The incurral of an illness or disability requiring the transfer to a different level of care. The permanent transfer rates and the temporary transfer rates together comprise the rate of morbidity.

2.19 Non-Contractual Resident

A person living in the CCRC without a health care guarantee and without a refund guarantee. Non-contractual residents normally pay for all health care services received on a fee for service basis. Examples of non-contractual residents are rental or lease residents, and direct admissions to the health center.

2.20 Occupancy Rate

The number of occupied units at each level of care by contractual and non-contractual residents, relative to available units.

2.21 Periodic Fee

Amounts payable periodically (usually monthly) by a contractual resident or member. The amounts are typically adjusted from time to time to reflect changes in operating costs.

2.22 Permanent Transfer

A move from one level of care to another level of care without expectation of returning to the former level of care.

2.23 Physical Property

Physical assets, such as land, building, furniture, fixtures, or equipment. These assets, excluding land, are assumed to depreciate over their respective lifetimes. These assets are also referred to as the fixed assets.

2.24 Population Projection

An estimate of the expected number of contractual residents or members at various future times.

2.25 Refund Guarantee

A clause in a residency agreement or membership agreement that provides for a refund of any portion of the advance fee upon termination of the agreement.

2.26 Residency Agreement

A contract between one or more residents and a CCRC that includes a health care guarantee or a refund guarantee, and describes the services to be provided and the obligations of the parties. The contract is usually of long duration and may be for the life of each contractual resident.

2.27 Temporary Transfer

A move from one level of care to another level of care with the expectation of returning to the former level of care.

2.28 Trend

Measure of rates of change, over time, that affects revenues, costs, or actuarial assumptions.

2.29 Valuation Date

The date as of which the assets and liabilities of the CCRC or At Home Program are estimated.

2.30 Withdrawal

The termination of a residency agreement or membership agreement by the contractual resident or member for reasons other than death.

Section 3.Analysis of Issues and Recommended Practices

3.1 Introduction

When providing actuarial services related to CCRCs or At Home Programs, the actuary should take into account the relevant financial items associated with the organizations, current contractual residents or members, new contractual residents or members, and levels of care provided, as well as relevant residency agreement or membership agreement provisions and applicable law. The actuary should use methods and assumptions that are, in the actuary’s professional judgment, appropriate considering the scope and purpose of the assignment.

3.2 Determination of Satisfactory Actuarial Balance

In determining whether the CCRC or At Home Program is in satisfactory actuarial balance as of the valuation date, the actuary should evaluate whether the CCRC or At Home Program meets all of the following three conditions:

3.2.1 Condition 1: Adequate Resources for Current Contractual Residents or Members

The resources available to current contractual residents or members include any existing net assets plus the actuarial present value of future revenues, such as periodic fees, additional fees, and third-party payments (for example, Medicare, Medicaid, and long-term care insurance).

Condition 1 would be met if the resources are greater than or equal to any existing liabilities for the current contractual residents or members plus the actuarial present value of the expected costs associated with the contractual obligations to current contractual residents or members. The actuary should determine if this condition is satisfied using the actuarial balance sheet (see section 3.3).

3.2.2 Condition 2: Adequate Fee Structure for a Cohort of New Contractual Residents or New Members

For a cohort of new contractual residents or new members, the expected fees are the sum of the advance fees paid plus the actuarial present value of the new contractual residents’ or new members’ expected future revenues, such as periodic fees, additional fees, and third-party payments (for example, Medicare, Medicaid, and long-term care insurance).

Condition 2 would be met if the expected fees are greater than or equal to the actuarial present value of the costs associated with the contractual obligations determined at an appropriate occupancy or membership date for the cohort. The actuary should determine if this condition is satisfied using the cohort pricing analysis (see section 3.4).

3.2.3 Condition 3: Positive Projected Cash and Investment Balances

The projection of cash and investment balances over the projection period should include revenue and expenses from all known sources, including current contractual residents or members, new contractual residents or members, and any non-contractual residents.

The actuary should choose a projection period that extends to a point at which, in the actuary’s professional judgment, the use of a longer period would not materially affect the results and conclusions.

Condition 3 would be met if the cash and investment balances are positive in each projection year. The actuary should determine whether this condition is satisfied using the cash flow projection (see section 3.5).

In the event the CCRC or At Home Program fails to meet any of the three conditions as specified above, the actuary should consult with the organization to address possible corrective actions to achieve satisfactory actuarial balance.

For a proposed or start-up CCRC or At Home Program, the actuary should evaluate conditions 1 and 2 using a future valuation date and should begin evaluating condition 3 as of a future date. The actuary should select such future dates that are consistent with the end of the start-up period. For example, the actuary may evaluate these conditions using the earlier of a short-term period (such as three to five years) after opening or when the CCRC or At Home Program reaches the targeted number of contractual residents or members.

3.3 Actuarial Balance Sheet

The actuary should develop the actuarial balance sheet according to the following:

3.3.1 Closed-Group Projection of Current Contractual Residents or Members

The actuary should use a population projection that is performed solely with respect to current contractual residents or members on the valuation date. The actuary should project the surviving contractual residents’ or members’ movements through various levels of care until contract termination. This projection excludes new contractual residents, new members, and any non-contractual residents.

3.3.2 Assets

The actuary should estimate the actuarial present value of each of the following: the future periodic fees (described in section 3.6.1), the future additional fees and third-party payments (described in section 3.6.2), and the physical property for assets currently in service (described in section 3.6.3).

The actuary should reflect in the actuarial balance sheet other assets from the accounting balance sheet as appropriate, in the actuary’s professional judgment. These assets generally include such items as cash and investment balances, current receivables, and other items not specifically reflected in the above guidance.

3.3.3 Liabilities

The actuary should estimate the actuarial present value of each of the following: the future use of physical property (described in section 3.6.4), the future operating expenses (described in section 3.6.5), the future refunds due to refund guarantees (described in section 3.6.6), and the long-term debt (described in section 3.6.7).

The actuary should reflect in the actuarial balance sheet other liabilities from the accounting balance sheet as appropriate, in the actuary’s professional judgment. These liabilities generally include such items as current payables, prepaid contractual resident or member deposits, fees paid in advance, short-term debt obligations, and other items not specifically reflected in the above guidance.

3.4 Cohort Pricing Analysis

The actuary should develop the cohort pricing analysis based on the actuarial present value of revenues and expenses associated with a cohort of new contractual residents or new members.

The actuary should use a population projection that is performed solely with respect to a cohort of new contractual residents or new members. The actuary should project surviving contractual resident or member movements through various levels of care until contract termination. This population projection excludes any non-contractual residents.

The revenues include the advance fees, the actuarial present value of future periodic fees (described in section 3.6.1), and the actuarial present value of future additional fees and third-party payments (described in section 3.6.2).

The expenses include the actuarial present value of each of the following: the future use of physical property (described in section 3.6.4), the future operating expenses (described in section 3.6.5), and the future refunds due to refund guarantees (described in section 3.6.6).

The actuary may consider, subject to disclosure, the use of expense levels consistent with the targeted number of contractual residents or members when a material change in the population, such as growth resulting from new construction or expansion, is expected.

3.5 Cash Flow Projections

The actuary should perform cash flow projections using an open group population projection that includes existing contractual residents or members on the valuation date together with expected future contractual residents or members consistent with assumed occupancy rates and membership levels. For CCRCs, the actuary should include non-contractual residents in this population projection that use unoccupied units or beds in various levels of care consistent with assumed occupancy rates.

The actuary should select assumptions in the cash flow projections that are consistent with those used in the development of the actuarial balance sheet and cohort pricing analysis (see sections 3.3 and 3.4).

The actuary should reflect revenues from all known sources (such as advance fees, periodic fees, additional fees, payments from non-contractual residents, third-party payments, and investment income). The actuary should reflect expenses from all known sources (such as operating expenses, capital expenditures, debt interest and principal payments, any cost of using an offsite health facility, and refunds due to refund guarantees).

In the cash flow projection, the actuary should develop the cash and investment balances at the beginning and end of each projection year.

3.6 Actuarial Asset and Liability Values

When developing the actuarial balance sheet or the cohort pricing analysis, the actuary should develop the following actuarial present value items.

3.6.1 Future Periodic Fees

The actuary should estimate the actuarial present value of future periodic fees by projecting the fees payable by the surviving contractual residents or members of the appropriate closed-group population in each level of care in each future year, and discounted to the valuation date. In the estimate of future fees, the actuary should reflect current rates adjusted for projected future fee increases.

3.6.2 Future Additional Fees and Third-Party Payments

The actuary should estimate the actuarial present value of future additional fees (such as guest meals and additional meals) and third-party payments. When projecting future payments, the actuary should project the additional revenue payable by, or on behalf of, the surviving contractual residents or members attributable to the appropriate closed-group population in each level of care in each future year. In the estimate of these future payments, the actuary should reflect current experience adjusted for projected future increases.

3.6.3 Physical Property for Assets Currently in Service

The actuary should estimate the actuarial present value of physical property for assets currently in service as the actuarial present value of the projected remaining annual capital expense charges associated with assets in service as of the valuation date.

The actuary should estimate the annual capital expense charge for the use of an asset for each year using its useful lifetime. The projected annual capital expense charge consists of the imputed interest charge for the use of the asset plus the change in asset value from one year to the next. In calculating the capital expense charges, the actuary should use a rate consistent with the cost of capital at the time the asset was originally put into service or the cost of capital in the current economic environment.

3.6.4 Future Use of Physical Property

The actuary should estimate the actuarial present value of the future use of physical property by taking the projected annual capital expense charges for both the current and replacement fixed assets allocated to the surviving contractual residents of the appropriate closed-group population in each future year and discounting the result back to the valuation date. The actuary should consider developing the actuarial present value estimates for each level of care.

The actuary should use a methodology to estimate the annual capital expense charges that is consistent with the methodology used to estimate the annual capital expense charges of physical property for assets currently in service (see section 3.6.3).

3.6.5 Future Operating Expenses

The actuary should estimate the actuarial present value of future operating expenses by taking the operating expenses allocated to the contractual residents or members of the appropriate closed-group population in each future year and discounting the result back to the valuation date. The actuary should exclude from future operating expenses (a) future capital expenditures, which are discussed in section 3.6.4; and (b) the future long-term debt interest and principal payments, which are discussed in section 3.6.7.

When estimating future operating expenses, the actuary should reflect future cost trends and reflect underlying expense consumption patterns in the allocation. The actuary should allocate expenses across the various levels of care and within each level of care on an appropriate basis such as per person, per unit, or per square foot.

3.6.6 Future Refunds Due to Refund Guarantees

The actuary should estimate the actuarial present value of future refunds due to refund guarantees by estimating the amount of refund due to each terminating contractual resident or member of the appropriate closed-group population in each future year and discounting the amounts back to the valuation date. The refund calculation is for the contractual amount of the advance fee refund. The actuary should calculate the estimate of the advance fee refund based on the contractual liability for each future year on the terms of the residency agreement or membership agreement assumed to be applicable to that contractual resident or member and the organization’s actual practice, if any, with regard to payment of refunds.

3.6.7 Long-Term Debt

The actuary should estimate the present value of long-term debt as the discounted value of the projected remaining principal and interest payments as of the valuation date. The present value of long-term debt may be different than the amount on the accounting balance sheet depending on the relationship between the discount rate and the actual or expected interest rate on the debt.

3.7 Selection of Actuarial Assumptions

The actuary should take into account the following when selecting assumptions.

3.7.1 Actuarial Assumptions

In selecting actuarial assumptions for mortality, morbidity, withdrawal, and occupancy rates, the actuary should reflect each of the following as appropriate:

- age and gender;

- health characteristics;

- permanent transfer and temporary transfer patterns;

- level of care status and expected differences in experience between contractual residents or members in different levels of care;

- time elapsed since the last change in the level of care;

- single or joint contracts;

- demographic profile and number of new contractual residents or members;

- time elapsed since the contractual resident or member entered the CCRC or At Home Program;

- actual experience of the CCRC or At Home Program, and the credibility of the experience;

- contractual guarantees, such as health care guarantees and refund guarantees; and

- operational policies and practices of the organization, such as transfer policies.

The actuary should select trend assumptions to project mortality (sometimes referred to as “mortality improvement,” which can be positive or negative), morbidity, withdrawal, and occupancy rates that are reasonable, in the actuary’s professional judgment. In selecting trend assumptions, the actuary should consider and review appropriate data. The data may include trend experience studies, appropriate industry studies, and management occupancy rate projections.

3.7.2 Trend Assumptions for Fees and Expenses

The actuary should set trend assumptions for periodic fees, advance fees, additional fees, and other revenue items. The actuary should also set trend assumptions for operating expenses, capital expenditures, and other expense items. The actuary may use different trend assumptions, as appropriate, for various categories of revenues and expenses. In setting trend assumptions for periodic fees, the actuary should also take into account practical, competitive, and contractual considerations.

The actuary should select assumptions for future trends in periodic fees that are consistent with the trend assumptions that are used in projecting future expenses. If the actuary uses different trend assumptions for periodic fees and operating expenses, the actuary should disclose this difference.

3.7.3 Investment Rate and Discount Rate Assumptions

The actuary should select investment rate and discount rate assumptions that are individually reasonable, mutually consistent, and reflective of the long-term nature of the residency agreement or membership agreement as follows:

- short- and long-term market expectations, and the future investment strategy of the organization to estimate investment income for the cash flow projection; and

- discount rate to estimate actuarial present values that, in the actuary’s professional judgment, is reasonable and appropriate, and is consistent with the investment rate.

3.7.4 Revenue and Expense Allocation Assumptions

The actuary should assume an allocation of general revenues and expenses to the various levels of care, and to current and new contractual residents or members. The actuary should determine whether the sum of all allocated expenses reconciles to the total projected expenses of the CCRC or At Home Program.

3.7.5 Going-Concern Assumption

The actuarial balance sheet, the cohort pricing analysis, and the cash flow projection rely on assumptions predicated on the ongoing financial viability and continuation of the CCRC or At Home Program. This implies that the organization will be able to maintain appropriate occupancy rates or membership levels by attracting new contractual residents or members to replace existing contractual residents or members. The actuary should assess the ability of the organization to attract new contractual residents or members or any other known, significant circumstances that, in the actuary’s professional judgment, may affect the organization’s ability to remain a going concern.

3.7.6 Reasonableness of Assumptions

The actuary should review the assumptions for reasonableness. The assumptions should be reasonable, in the actuary’s professional judgment, in the aggregate and for each assumption individually. The actuary should identify material changes in assumptions, and methods relating to the use of those assumptions, compared to the most recent prior analysis if applicable.

In reviewing the assumptions for reasonableness, the actuary should take into account the following:

- the intended purpose of the measurement;

- the frequency with which the projections are expected to be updated;

- the length of the projection period;

- the sensitivity of the projections to the effect of variations in key actuarial assumptions;

- the potential variability of the assumption;

- consistency among related assumptions;

- the size of the CCRC’s contractual resident population or At Home Program membership;

- the ability to increase fees or decrease expenses in future periods;

- the level of capital available to provide for adverse fluctuation;

- any significant margins for uncertainty that have been included in the actuarial assumptions; and

- the expectation of no material bias (i.e., it is not materially optimistic or pessimistic) relative to the purpose of the measurement, excluding the effect of a margin.

3.8 Benevolence Funds and Financial Assistance Subsidies

The actuary should determine the benevolence funds or financial assistance subsidies available as well as the potential future liabilities for contractual residents or members who do not pay the contractual fees. For example, some organizations may set aside assets or funds from charitable contributions to assist contractual residents or members, while other organizations may include the costs of any assistance in the basic fee structure.

3.9 For-Profit CCRCs or At Home Programs

When performing actuarial services with respect to for-profit organizations, the actuary should determine the nature and financial implications of the ownership arrangement, including owner’s equity, past and possible future equity distributions, potential income tax liability, and historical and future capital expenditures funded by the owner.

3.10 Equity or Cooperative CCRCs or At Home Programs

When performing actuarial services with respect to equity or cooperative CCRCs or At Home Programs, the actuary should determine the nature and financial implications of any contractual resident or member ownership arrangement, including advance fee payments and refunds due to refund guarantees, and the value of assets invested in the physical property and the replacement costs of these fixed assets.

3.11 Additional Considerations Affecting CCRC or At Home Program Finances

The actuary should determine the scope of the organization’s commitments to current and prospective contractual residents or members and the nature of its fee structure. The actuary may obtain this information from the applicable residency agreements or membership agreements and any other reasonable source of information about the organization. When interpreting these documents, the actuary should determine the following:

- the admission and underwriting criteria and how they are applied;

- the terms of the residency agreement or membership agreement and any limitations on the period for which commitments are made;

- any known, significant limitations on the organization’s ability to change future periodic fees;

- any refund guarantees;

- any limitation on the services provided and any collectability risk for services limited under the contract or requiring additional payment;

- any contract provisions for prepaid health care or for additional charges if a contractual resident or member receives health care;

- any affiliation with another entity and the extent to which any such entity would assume responsibility for the organization’s obligations; and

- any other matter that, in the actuary’s professional judgment, is expected to have a material effect on the organization’s current or future financial statements.

3.12 External Restrictions

The actuary should take into account restrictions on the CCRC or At Home Program from external sources, such as applicable law, regulation, or other binding authority. Examples include a state’s Medicaid reimbursement policy, regulations restricting the use of health center beds by non-contractual residents, and any relevant lender-imposed restrictions.

3.13 Reliance on Data or Other Information Supplied by Others

When relying on data or other information supplied by others, the actuary should refer to ASOP No. 23, Data Quality, and ASOP No. 41, Actuarial Communications, for guidance.

3.14 Documentation

The actuary should consider preparing and retaining documentation to support compliance with the requirements of section 3 and the disclosure requirements of section 4. When preparing documentation, the actuary should prepare documentation in a form such that another actuary qualified in the same practice area could assess the reasonableness of the actuary’s work. The degree of such documentation should be based on the professional judgment of the actuary and may vary with the complexity and purpose of the actuarial services. In addition, the actuary should refer to ASOP No. 41 for guidance related to the retention of file material other than that which is to be disclosed under section 4.

Section 4. Communications and Disclosures

4.1 Required Disclosures in an Actuarial Report

When issuing an actuarial report to which this standard applies, the actuary should refer to ASOP Nos. 23 and 41. In addition, the actuary should disclose the following in such actuarial reports, if applicable:

- historical and current financial data used to produce the actuarial balance sheet, cohort pricing analysis, and cash flow projections, in accordance with sections 3.3, 3.4, and 3.5;

- summary of historical contractual resident or member data and population statistics for contractual residents or members as of the valuation date, in accordance with sections 3.3, 3.4, and 3.5;

- assumptions and methodology used in performing the population projections, in accordance with sections 3.3, 3.4, and 3.5;

- assumed expense levels consistent with the targeted number of contractual residents or members when a material change in the population is expected, in accordance with section 3.4;

- assumptions and methodology used to estimate each actuarial present value, in accordance with section 3.6;

- assumptions and methodology used to value and depreciate the physical property, in accordance with sections 3.6.3 and 3.6.4;

- mortality, morbidity, withdrawal, and occupancy rate assumptions (including trend assumptions, if any), and methodology used in selecting such assumptions, in accordance with sections 3.7.1;

- trend rates for revenues and expenses, and the relationship between the two, in accordance with section 3.7.2;

- investment rate and discount rate, in accordance with section 3.7.3;

- assumptions and methodology used to allocate general revenue an expenses, in accordance with section 3.7.4;

- any known significant circumstances that may affect the organization’s ability to remain a going concern, in accordance with section 3.7.5;

- assumptions and methodology used for any significant margin for uncertainty, or a similar adjustment or provision, included in the actuarial valuation, including any significant assumptions affecting the valuation regarding surplus available to provide for adverse fluctuations, in accordance with section 3.7.6;

- any material changes in assumptions or methods from the most recent prior analysis, in accordance with section 3.7.6;

- the results of any sensitivity tests performed, in accordance with section 3.7.6; and

- any assistance assumed to be derived from dedicated benevolence funds or financial assistance subsidies, in accordance with section 3.8.

4.2 Assignments Involving an Opinion on Satisfactory Actuarial Balance

The actuarial report should disclose the actuarial balance sheet, the cohort pricing analysis, and the cash and investment balances at the beginning and end of each projection year, which were prepared to test the three conditions, in accordance with sections 3.3, 3.4, and 3.5 and state whether or not each condition is met.

If one or more of the three conditions is not met, the actuary should disclose the implications of the deficiency and, if known, a description of management’s plans to address the deficiency for each unmet condition.

If the actuary is unable to form the needed opinion regarding whether the organization is in satisfactory actuarial balance, or if the opinion is adverse (due to failing one or more of the conditions) or otherwise qualified, then the actuary should disclose why the actuary is unable to form an unqualified favorable opinion.

4.3 Additional Disclosures in an Actuarial Report

The actuary also should include disclosures in accordance with ASOP No. 41 in an actuarial report for the following circumstances:

- if any material assumption or method was prescribed by applicable law;

- if the actuary states reliance on other sources and thereby disclaims responsibility for any material assumption or method selected by a party other than the actuary; and

- if in the actuary’s professional judgment, the actuary has deviated materially from the guidance of this ASOP.

Appendix 1: Background and Current Practices

Note: This appendix is provided for informational purposes and is not part of the standard of practice.

Background

Certain contractual obligations of a CCRC or At Home Programs are contingent upon the occurrence, timing, and duration of certain future events. The CCRC contractual resident or At Home Program member typically pays for such future promised services through a combination of advance and periodic fees, typically before the services are provided. Actuarial methods are used to establish the fee structure and to measure the organization’s liabilities for the provision of future promised services.

High occupancy, sound pricing, care management, and effective financial management are some of the keys to the successful operation of a CCRC. The ability of a CCRC to attract new contractual residents to fill vacancies will depend on keeping the CCRC competitive with respect to its physical property, its fee schedule, and the general attractiveness of its whole environment. Membership levels, sound pricing, care management, and effective financial management are some of the keys to the successful operation of an At Home Program.

Current Practices

Current actuarial practices for CCRCs are generally now well established. Prior to the release of the first edition of this ASOP and the release of subsequent educational material by various entities, actuaries used differing analytical approaches. These approaches included differing methods to determine closed and open-group contractual resident projections, projected refunds due to refund guarantees, physical property valuations, long-term debt, and other items. While historically differences did exist, these differences have now mostly been eliminated and standardized practices have evolved.

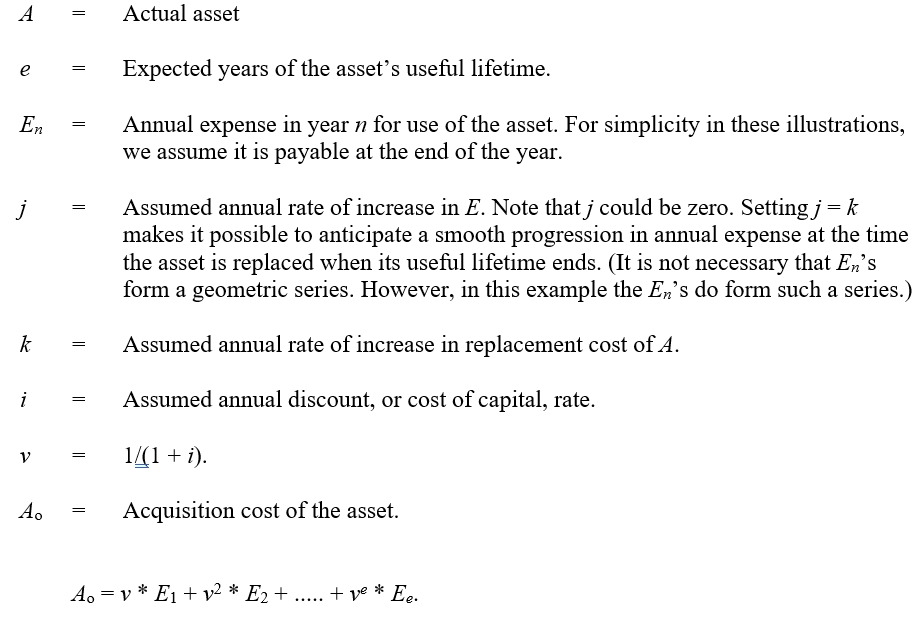

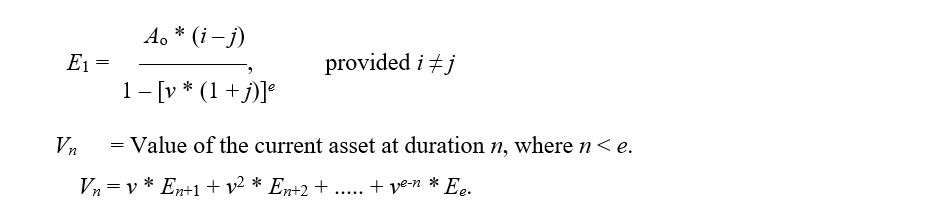

Illustrative Capital Expense Charge Development and Physical Property Valuation

The physical property, or fixed assets, of a CCRC are a significant asset of the CCRC, and also a significant cost to the contractual residents of the CCRC. In order to provide for equity among generations of contractual residents, it is necessary to allocate an appropriate part of the cost of the use of physical property to current contractual residents as of the valuation date and to the cohort of new contractual residents.

The method described in this appendix for developing and assigning the annual capital expense charge for asset use, determining the asset’s actuarial value, and determining the liability for asset use is one illustrative method designed to provide for equity among generations of contractual residents. (Illustrative formulas for expensing and valuing physical property are presented at the end of this appendix.)

Physical property assets may be valued and depreciated using level, decreasing, or increasing depreciation methodologies based on actuarial principles, the nature of the underlying assets, and other factors.

Capital Expense (Imputed Interest plus Depreciation) Charges—The annual capital expense charge for physical property consists of the imputed interest for the use of the asset, or opportunity cost of using cash resources for purchasing a fixed asset (because it is not an interest-earning investment), plus the change in asset value from one year to the next.

- Each item of physical property is assigned an assumed useful lifetime and an appropriate rate of inflation. While GAAP expected lifetimes might be available, alternative lifetimes may be available from other sources such as engineering studies performed by the client. In the case of land, the expected useful lifetime may be perpetual.

- The annual capital expense charge for the use of an asset is developed for each year using its useful lifetime and is calculated as one of a series of annual amounts. The present value of this series, discounted to the time of acquisition, equals the cost of the asset. This series of annual amounts may be decreasing, level, or increasing.

- In similar fashion, capital expense charges are developed for physical property assumed to be purchased in future years. It is assumed that each asset will be replaced at the end of its useful lifetime with a new asset. The cost of the new asset is assumed to equal the original cost indexed for inflation. The asset is continually replaced at the end of successive useful lifetimes.An approximation of these replacement costs that better reflects the expected magnitude and timing of future capital expenditures may also be used. These approximations reflect a sufficient level of future capital expenditures necessary to maintain the physical property for future use.

Capital expense charges are developed for the following items:

- Actuarial Value of Physical Property for Assets Currently in Service—Reflected as an asset on the actuarial balance sheet;

- Actuarial Present Value of Future Use of Physical Property Consumed by Current Contractual residents throughout Their Respective Lifetimes—Reflected as a liability on the actuarial balance sheet; and

- Actuarial Present Value for Future Use of Physical Property Consumed by a Hypothetical Group of Prospective Contractual Residents—Reflected as a liability on the cohort pricing analysis.

Value of Physical Property for Assets Currently in Service—The actuarial value of each asset is the discounted value (without survivorship) of the remaining annual capital expense charges as of the valuation date. The sum of these values for all such assets in service as of the valuation date is reflected as an asset on the actuarial balance sheet.

Value of Future Use of Physical Property for Existing Contractual Residents—The actuarial present value of the future use of physical property for existing contractual residents is the discounted value (with survivorship) of the annual capital expense charges for the physical property, and its replacements, allocated to existing contractual residents as of the valuation date.

- The part of each future year’s capital expense charge that relates to the existing contractual residents as of the valuation date is determined by estimating the ratio of the existing contractual resident survivorship group use to total CCRC use. The ratio may be in proportion to population, number of CCRC occupied beds or units, square footage, or some other appropriate measure. For years during fill-up or material change in population, it may be appropriate to substitute a target or ultimate level of use for the actual estimated level of total use.

- The current actuarial liability for the promised future use of a physical asset (and its replacements) with respect to the existing contractual resident closed group is the sum (for all years) of the part of such capital expense charge in each future year related to the existing closed group, as determined in (a), discounted to the valuation date.

Value of Future Use of Physical Property for the New Entrant Cohort—The actuarial present value of the future use of physical property for the new entrant cohort is the discounted value (with survivorship) of the annual capital expense charges for the physical property, and its replacements, allocated to the new entrant cohort closed group.

- The part of each future year’s capital expense charge that relates to the new entrant cohort is determined by estimating the ratio of the new entrant cohort survivorship group use to total CCRC use.

- The current actuarial liability for the promised future use of a physical asset (and its replacements) with respect to the new entrant cohort is the sum (for all years) of the part of such capital expense charge in each future year related to the new entrant cohort closed group, as determined in (a), discounted to the valuation date.

Illustrative Formulas for Expensing and Valuing Physical Property

Note: These formulas illustrate allocations on a per contractual resident basis. Other allocation bases such as units, beds, square footage, etc. may be more appropriate for certain assets.

A. Relationships of Asset Cost, Asset Value, and Open-Group Annual Expense

From this we obtain

From this we obtain

This shows that the annual expense for a physical asset consists of the interest that is forgone (because it is not an interest-earning investment), plus the change in asset value from one year to the next. In the case of land, the annual expense consists of only the interest that is forgone, since there is no assumed change in asset value (lifetime is perpetual).

B. Relationship of Closed-Group Liability with Open-Group Expense

Pn = Projected total population at duration n, determined on an open-group basis. Depending on the circumstances, a reasonable approximation for P may be a constant number equaling the current population.

Cn = Projected surviving population at duration n from a specified closed group. The closed group may be the closed group of current contractual residents or the closed group for a cohort of new contractual residents.

If a part of a given CCRC is used for persons not under contract, only the fraction devoted to those under contract should be considered. One way of accomplishing this is to include those not under contract in Pn but not in Cn.

Ln = Liability at duration n for the future use of the asset and its replacements by a specific closed group.

APPENDIX 2

COMMENTS ON THE EXPOSURE DRAFT AND RESPONSES

The exposure draft of the proposed revision of ASOP No. 3, Continuing Care Retirement Communities and At Home Programs, was issued in November 2020 with a comment deadline of February 1, 2021. Five comment letters were received, some of which were submitted on behalf of multiple commentators, such as by firms or committees. For purposes of this appendix, the term “commentator” may refer to more than one person associated with a particular comment letter. The ASOP No. 3 Task Force carefully considered all comments received, and the ASB reviewed (and modified, where appropriate) the changes proposed by the ASOP No. 3 Task Force and the ASB Health Committee.

Summarized here are the significant issues and questions contained in the comment letters and the responses. Minor wording or punctuation changes that were suggested but not significant are not reflected in the appendix, although they may have been adopted.

The term “reviewers” in appendix 2 includes the ASOP No. 3 Task Force, the ASB Health Committee, and the ASB. Also, the section numbers and titles used in appendix 2 refer to those in the exposure draft, which are then cross referenced with those in the final ASOP.

PDF Version: Download Here

Last Revised: September 2021

Effective Date: June 01, 2022

Document Number: 202

Document Status: Adopted