Proposed Actuarial Standard of Practice

Life Settlements Mortality

TRANSMITTAL MEMORANDUM

May 2013

TO: Members of Actuarial Organizations Governed by the Standards of Practice of the Actuarial Standards Board and Other Persons Interested in Reporting and Validation of Mortality used in Life Settlement Investments

FROM: Actuarial Standards Board (ASB)

SUBJ: Proposed Actuarial Standard of Practice (ASOP)

This document contains the exposure draft of a proposed actuarial standard of practice, Life Settlements Mortality. Please review this exposure draft and give the ASB the benefit of your comments and suggestions. Each written response and each response sent by e-mail to the address below will be acknowledged, and all responses will receive appropriate consideration by the drafting committee in preparing the final document for approval by the ASB.

The ASB accepts comments by either electronic or conventional mail. The preferred form is e-mail, as it eases the task of grouping comments by section. However, please feel free to use either form. If you wish to use e-mail, please send a message to comments@actuary.org. You may include your comments either in the body of the message or as an attachment prepared in any commonly used word processing format. Please do not password protect any attachments. Include the phrase “ASB COMMENTS” in the subject line of your message. Please note: Any message not containing this exact phrase in the subject line will be deleted by our system’s spam filter.

If you wish to use conventional mail, please send comments to the following address:

Life Settlements Mortality

Actuarial Standards Board

1850 M Street, Third Floor

Washington, DC 20036

The ASB posts all signed comments received to its website to encourage transparency and dialogue. Unsigned or anonymous comments will not be considered by the ASB nor posted to the website. The comments will not be edited, amended, or truncated in any way. Comments will be posted in the order that they are received. Comments will be removed when final action on a proposed standard is taken. The ASB website is a public website and all comments will be available to the general public. The ASB disclaims any responsibility for the content of the comments, which are solely the responsibility of those who submit them.

Deadline for receipt of responses in the ASB office: July 31, 2013

Background

The life settlements market arose from the viatical settlements market that grew quickly in the 1980s. Actuaries are involved in all aspects of the market, including (a) working with Life Expectancy (LE) providers to establish appropriate survival curves for risk appraisal, (b) determining a value for a buyer who wishes to purchase a specific life insurance policy or portfolio, and (c) valuing the policies in a portfolio for financial reporting purposes. An understanding of mortality assumptions and of how individual risk assessment affects the mortality assumptions for individual lives is critical to a proper actuarial valuation and risk analysis. To date, actuarial practices have varied widely in this market, and there are no specific regulatory standards defining life settlement mortality tables or assumptions.

The life settlements market has demanded actual-to-expected (A/E) results from the LE providers, but in the absence of specific guidelines and disclosures, practices for calculating A/E results have varied widely. A limited number of states require LE providers to file A/E ratios, but again, lack of specific guidelines has led to concerns with mortality tables and methodologies used. Legislation has been introduced in one state to discontinue filing requirements due to the lack of uniformity in reporting. At issue are survival curves defined for exposure measurement and methodologies for adjusting such curves to reflect individual risk assessments. Also, measurement of exposures based on multiple underwritings has posed significant difficulties.

At the time of the writing of this ASOP, revisions are under way to ASOP No. 25, Credibility Procedures Applicable to Accident and Health, Group Term Life, and Property/Casualty Coverages. While the currently applicable ASOP No. 25 applies only to accident and health, group term life, and property/casualty coverages, it is in the process of being revised to apply to all coverage types. If this revised ASOP, to be titled Credibility Procedures, is adopted by the ASB, it will be applicable for credibility work performed related to life settlements as defined in the scope of that standard.

Request for Comments

The ASB would appreciate comments on all areas of this proposed standard and would like to draw the readers’ attention to the following questions in particular:

1. Life expectancy providers may provide survival curves with their estimates. As drafted, this standard does not require disclosure when the actuary chooses a different survival curve assumption. Should it?

2. Methodologies for Actual-to-Expected studies for life settlements may vary depending on the purpose of the study. The task force chose to define a “historical method” as being distinct from any number of “modified methods.” Is this distinction clear? Is it clear when a historical method is required?

3. Are the disclosures required in this standard sufficient and clear?

4. One insured may have had multiple life expectancy estimates. Are the disclosures for handling this situation appropriate?

The ASB reviewed the draft and approved its exposure in May 2013.

Life Settlements Mortality Task Force

Timothy A. DeMars, Chairperson

Mary J. Bahna-Nolan Peter J. Bondy

Jeremy J. Brown Vincent J. Granieri

Linda M. Lankowski Scott E. Morrow

Arshad H. Qureshi Larry H. Rubin

Life Committee of the ASB

Jeremy J. Brown, Chairperson

David A. Bretlinger James B. Milholland

Dale S. Hagstrom David Y. Rogers

Qing Fang Alfred O. Weller

John B. Gould Candance J. Wood

Actuarial Standards Board

Robert G. Meilander, Chairperson

Beth E. Fitzgerald Thomas D. Levy

Alan D. Ford Patricia E. Matson

Patrick J. Grannan James J. Murphy

Stephen G. Kellison James F. Verlautz

The ASB establishes and improves standards of actuarial practice. These ASOPs identify what the actuary should consider, document, and disclose when performing an actuarial assignment. The ASB’s goal is to set standards for appropriate practice for the U.S.

Section 1. Purpose, Scope, Cross References, and Effective Date

1.1 Purpose

This actuarial standard of practice provides guidance to actuaries evaluating mortality assumptions and experience associated with life settlements.

1.2 Scope

This standard applies to actuaries performing professional services, when reporting on or evaluating mortality with respect to life settlements, or when analyzing or using mortality assumptions with respect to life settlements. If the actuary departs from the guidance set forth in this standard in order to comply with applicable law (statutes, regulations, and other legally binding authority), or for any other reason the actuary deems appropriate, the actuary should refer to section 4.

1.3 Cross References

When this standard refers to the provisions of other documents, the reference includes the referenced documents as they may be amended or restated in the future, and any success or to them, by whatever name called. If any amended or restated document differs materially from the originally referenced document, the actuary should consider the guidance in this standard to the extent it is applicable and appropriate.

1.4 Effective Date

This standard is effective for work performed on or after four months after adoption by the Actuarial Standards Board.

Section 2. Definitions

The terms below are defined for use in this actuarial standard of practice.

2.1 Actual-to-Expected (A/E) Ratio

Actual deaths (either face amount or number of lives) in a group of lives being evaluated over a specified period divided by the expected deaths over the same period.

2.2 Actual-to-Expected Analysis

The process of calculating and analyzing A/E ratios over a selected time period; for example, across different ages, genders and durations. This is also known as an A/E study.

2.3 Debits and Credits

The components of a system used by underwriters to determine a set of mortality multiples to apply to a base mortality table. Debits increase the mortality multiple due to various impairments that an insured may have while credits reduce the mortality multiple due to good health characteristics.

2.4 Duration

The length of time, measured in years, since a life expectancy estimate was issued.

2.5 Expected Deaths

The results of a calculation for a period obtained by applying the probabilities of death for each insured to the population of insureds exposed to the risk of death during the period.

2.6 Graduation

The process of making adjustments to experience results in order to have a smooth progression in the mortality rates over the whole age range.

2.7 Historical A/E Analysis

A/E analysis using the mortality tables, underwriting multipliers, improvement factors, medical records, and other pertinent information actually used when the life expectancy was issued.

2.8 Impairment

Health factor or condition that tends to increase an insured’s probability of death.

2.9 Impaired Mortality

Mortality assumption that has been adjusted for impairments.

2.10 Incurred but not Reported (IBNR) Deaths

Adjustment to observed deaths in a given time period to account for deaths that have occurred but have not been reported due to the time lag in reporting systems or errors and incomplete information available from reporting sources regarding deaths.

2.11 Incurred Claim

A death that has taken place, whether known or not known.

2.12 Insured

An individual whose life is covered by a life insurance policy.

2.13 Life Expectancy (LE)

The expected future lifetime of an insured. There are two primary types of life expectancies, mean and median, reported by LE providers in the life settlement market.

2.14 Life Expectancy Provider (LE Provider)

An entity, specializing in the assessment of older or impaired lives, that applies medical underwriting services to determine a mortality assumption or life expectancy. Sometimes referred to as the underwriter.

2.15 Life Settlement

The life insurance policy or policies sold to an investor. The term “life settlement” includes both viatical and other life settlements. A viatical life settlement is any life settlement where the insured has a life expectancy generally less than two to three years depending on state regulation.

2.16 Mean Life Expectancy

The average life expectancy. It is equal to the sum of all future probabilities of survival based on the assumed survival curve. The formula below is used to determine the life expectancy in months.

2.17 Median Life Expectancy

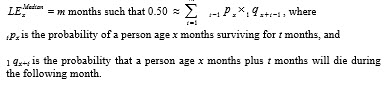

The point in time at which, based on the assumed survival curve, there is a 50% probability that the person will still be alive. The formula below is used to determine the life expectancy in months.

2.18 Modification Factor

A factor that is used to adjust standard mortality to reflect rating classification. This includes such items as flat extras, mortality multiples, and age ratings.

2.19 Modified A/E Analysis

Any A/E analysis, other than a historical A/E analysis, in which mortality assumptions differ from those originally used by the LE provider. This may result in life expectancy estimates that differ from those originally provided.

2.20 Mortality Assumption

The annual probability of death at each age and duration. This may reflect an assumption of future mortality improvement or deterioration or modification factors. This term may apply to either a single insured or group of insureds.

2.21 Mortality Multiple

A modification factor typically determined from a debit/credit underwriting methodology.

2.22 Survival Curve

The probability data set representing the assumed probability of survival to the end of every period in the future for an insured.

2.23 Underwriting

The process of evaluating medical and other information received on a given insured to determine modification factors reflecting risk classification for that insured.

Section 3. Analysis of Issues and Recommended Practices

3.1 Purpose of the Assignment

The actuary should know the purpose of the assignment and be familiar with any regulatory or accounting standards that may have a bearing on the actuary’s work product. Assignments that may result in different sets of mortality assumptions include fair value valuation (for example, under Accounting Standards Codification 820, Fair Value Measurements and Disclosures) and performing or using an A/E study.

3.2 Required Knowledge

The actuary should be knowledgeable about mortality table construction, exposure methods, mortality improvement, older age and impaired mortality, graduation, and related issues.

3.3 Developing Mortality Assumptions

When an actuary is developing mortality assumptions, the following apply.

3.3.1 Base Mortality Table Selection

The actuary should select a base mortality table that is appropriate for the purpose of the assignment. The actuary should choose a table (which may be a combination of tables), that in the actuary’s professional judgment reflects the characteristics of the underlying population. The actuary may use credible data to create new mortality tables if existing tables do not adequately fit the population. If the actuary uses a mortality table prescribed by another party or applicable law (statutes, regulations, and other legally binding authority), the actuary should refer to ASOP No. 41, section 3.4.4, and the disclosures in sections 4.1(f) and (g) of this ASOP.

3.3.2 Mortality TableModifications

The actuary should consider whether modifications to the base mortality table(s) are needed to fit the population being examined. In making these modifications, the actuary should consider items that may lead to a differentiation in mortality, such as socio-economic effect (i.e., a tendency for mortality rates to differ based on sociologic and economic factors), antiselection, selection period, impairment(s), impairment level, marketing methods, policies settled versus policies evaluated but not sold as life settlements, and variations in LE estimates provided by different LE providers.

3.3.3 Mortality Improvement or Deterioration

The actuary should consider whether incorporating historical and projected mortality improvement or deterioration is appropriate. These adjustments could be due to mortality improvement caused by medical advancements or new pharmaceutical drugs, which could cause a shift in expected mortality for a group of insureds within the population.

3.3.4 Application of Individual Underwriting to Mortality Assumptions

If the actuary has access to underwriting information on individual insureds in the population, the actuary should consider making adjustments to the mortality assumptions to reflect this information. The actuary should consider using available data regarding factors such as the impairment(s), impairment level, debits or credits assigned, mortality multiples, and life expectancies and their associated survival curves, as appropriate for the purpose of the assignment.

If life expectancies are used, the actuary should understand the basis for the life expectancies including whether the LE information provided is a mean or median LE.

3.3.5 Mortality Assumption Adjustments Using A/E Analysis

The actuary should consider adjusting mortality assumptions when A/E results are available.

3.4 Actual-to-Expected Analysis

When performing an A/E analysis, the actuary should produce results by duration. As data and credibility allow, the actuary should analyze results by gender, smoking class, age bands, level of mortality multiples, impairment type, and other pertinent categories.

3.4.1 Incurred Claims

The actuary should be aware of the methodology and sources used in determining incurred claims and the completeness of such approach for determining claims. The actuary should consider adjusting actual results to reflect IBNR deaths. The actuary should consider using a supplemental external source of recorded deaths, such as the Social Security Death Master File, if available, to improve the timeliness of reported deaths.

3.4.2 Multiple Life Expectancies for a Single Life

The actuary should assess whether the method for handling data regarding an insured underwritten multiple times (and creating multiple exposures) is appropriate for the intended use of the A/E study, given the reasons a specific insured was underwritten more than once. If the actuary uses a method prescribed by another party, the actuary should refer to ASOP No. 41, section 3.4.4, and the disclosures in section 4.1(f) and (g) of this ASOP.

3.4.3 Use of a Modified A/E Analysis

The actuary may analyze results based on a historical A/E analysis or a modified method. If a modified A/E method is used, a historical A/E analysis should be prepared for comparative purposes, if the necessary data are available.

3.5 Reliance on Data or Other Information Supplied by Others

When relying on data or other information supplied by others, the actuary should refer to ASOP No. 23, Data Quality, for guidance.

3.6 Credibility of Data Used in Evaluation of Mortality

When considering the credibility of the data used in setting assumptions, the actuary should refer to ASOP No. 25, Credibility Procedures Applicable to Accident and Health, Group Term Life, and Property/Casualty Coverages, for guidance.

3.7 Documentation

The actuary should prepare and retain documentation in compliance with the requirements of ASOP No. 41, Actuarial Communications. The actuary should also prepare and retain documentation to demonstrate compliance with the disclosure requirements of section 4.

Section 4. Communications and Disclosures

4.1 Disclosures

When issuing actuarial communications relating to mortality in life settlements, the actuary should refer to ASOP Nos. 23, 25, and 41. In addition, the actuary should disclose the following items:

a. any modifications to the mortality assumptions to reflect risk characteristics;

b. the extent of historical or projected mortality improvement or deterioration assumed for the assignment (section 3.3.3);

c. the method used for determining incurred claims, including any IBNR assumption, and discussion of the significance of such IBNR assumption;

d. any unresolved concerns the actuary may have about the data, assumptions used, or methodology used that could have a material impact on the actuarial work product;

e. the mortality assumption for estimating what a third party (market) would pay to purchase the asset, and the basis for that assumption, when performing work related to fair-value projections;

f. the disclosure in ASOP No. 41, section 4.2, if any material assumption or method was prescribed by applicable law (statutes,regulations, and other legally binding authority);

g. the disclosure in ASOP No. 41, section 4.3, if the actuary states reliance on other sources and thereby disclaims responsibility for any material assumption or method selected by a party other than the actuary; and the disclosure in ASOP No. 41, section 4.4, if, in the actuary’s professional judgment, the actuary has otherwise deviated materially from the guidance of this ASOP.

4.2 Disclosures when Performing an A/E Analysis

In addition to the disclosures in section 4.1, the actuary should disclose the following items if an A/E analysis is performed:

a. the source of the expected mortality table(s) and why the actuary believes they were appropriate for the assignment;

b. results of the A/E analysis by duration;

c. as data and credibility allow, a presentation of results by gender, smoking class, age bands, level of mortality multiples, impairment type and other pertinent categories;

d. whether the historical method or a modified method was used for the A/E analysis. Such disclosure should indicate the implications of the method, the reasons for the choice of method, and whether the method could distort the results of the analysis;

e. if modified A/E analysis results are being presented, a presentation of historical A/E analysis results for comparative purposes, if the necessary data are available;

f. a description of the methods used to adjust results for the impact of multiple life expectancy evaluations on the same insured or on the same policy;

g. a description of the methods used to adjust results for the impact of multiple policies on the same insured;

h. when IBNR is included in the analysis, a presentation of results with and without IBNR; and

i. a statement that A/E results that may not be indicative of future results.

Appendix

Background and Current Practices

Note: This appendix is provided for informational purposes but is not part of the standard of practice.

Background

Life Settlements are financial transactions in which a third party buys an existing life insurance policy for more than its cash surrender value but less than its net death benefit. The life settlements market grew out of the viatical market, where chronically ill AIDS patients sold their policies, often to individual investors. The viatical settlement market essentially ended with the advent of antiretroviral drugs, which extended the lives of AIDS patients, lowering the economic value of their life insurance policies. From there, the market focus shifted to other health impaired policyholders, primarily at older attained ages.

In the life settlement market, a mortality assumption is determined that allows the buyer to project expected premiums, death benefits, and other relevant cash flows period by period. These expected cash flows are then discounted to determine the policy value. To determine the mortality assumption for an insured, it is common to use life expectancy (LE) estimates produced by LE providers. The accuracy of the LE estimates is of great interest to the life settlement market since the value of a policy is highly dependent on the mortality assumption derived based on the LE estimate.

The life settlement market is highly dependent on actuarial expertise. In particular, analysis of actual mortality experience as compared to expectations (actual/expected or A/E analysis) has generated controversy in the life settlements market.

An A/E study is a backward looking evaluation of underwriting results based on assumed mortality. The mortality assumption may be based on the mortality tables and modification factors used to produce the original LE estimate. At times, the mortality assumptions maybe modified to reflect factors relevant to current LE estimate so that past results may be measured against current underwriting methodologies and tables.

Current Practices

Actuaries working in the life settlement market have been asked to assess mortality for many different purposes. These purposes include:

- A/E study of a LE provider

- Determining survival curves for a LE provider

- Pricing/modeling of life settlement policies and portfolios on behalf of investors

- Valuation for financial reporting

- Risk models to examine extension risk and its consequences for investor performance

In performing an A/E study on a block of lives or policies, there are several options for creating mortality assumptions for individual lives. The analyses differ regarding whether or not the original LE provider’s mortality assumption is adjusted. A historical A/E analysis uses the original LE provider’s mortality assumption. Two modified A/E analyses being used today are as follows:

1. Adjusted to Current Methodology A/E analysis– A/E analysis that typically defines expected deaths using mortality tables, underwriting multipliers, improvement factors and any other aspects of the underwriter’s current methodology applied to the medical records and any other pertinent information for each insured that existed at the time the insured was underwritten. This attempts to address the question of how accurate the LE provider’s estimates are today.

2. Back-solving the actual LE into a mortality table– A/E analysis that defines expected deaths by using the back-solving method with the actual LE that was issued and mortality assumptions that may or may not have actually been used when the LE was issued by the LE provider. This has commonly been used when the LE provider’s table is proprietary, non-existent, deemed not relevant, or in the actuary’s judgment is not appropriate for the life settlement population being studied.

In performing an A/E study, there are several methods that are used to handle multiple underwriting opinions on individual lives. The results of the A/E study can vary substantially depending on the method chosen. Some of the methods in use today are as follows:

1. Earliest submission – Counts only the earliest LE estimate produced for each insured. As a result, no single insured counts more than any other. This method does not reflect all instances of underwriting.

2. Latest submission – Counts only the latest LE estimate produced for each insured. Considerations are the same as in method 1. The main deficiency in using this method is that it excludes time periods where it is known that no deaths occurred. This may cause an increase to the A/E ratio.

3. One year look-back – Includes only the latest LE estimate within each calendar year.

4. Fractional method – The earliest LE estimate contributes one exposure up until the time that the insured is underwritten a second time, at which point each contributes half an exposure. Repeat as necessary. Only one total exposure per year perinsured is used, and a subject only contributes one death in the calculation.

5. Non-fractional method – Several LE estimates may be used for one insured. Possible reasons for inclusion depend on time elapsed since prior LE opinion used or material change in health status. One insured that has been underwritten many times may have a much larger impact on the A/E results than another insured that was underwritten once.

For A/E studies, there have been a wide range of adjustments made to account for IBNR. The level of IBNR chosen is crucial since the results of the A/E analysis could vary substantially. Given the age of the life settlement market, data availability, and the reliability of the methods used to determine deaths that have occurred, determining the appropriate IBNR level is difficult.

To the extent experience is available, a lag study is sometimes performed on the historical level of IBNR experienced. The results of the lag study, to the extent credible, are then used to determine the level of IBNR. Often a lag study is not feasible. In utilizing other resources in determining the level of IBNR, such as social security information, some practitioners account for differences in the population of life settlement participants, compared to the population being considered. A further problem is that the methodologies for determining maturities may change over time, as has happened when access to the Social Security Death Master File became more restricted.

In performing A/E studies in the life settlement market, the methods used to measure exposure vary. The methods differ in the measurement of expected deaths during a period in which death occurs,or the insured or policy leaves the study. Three methods commonly used are as follows:

1. Scheduled – This method includes the expected deaths for the lesser of the entire duration and the end of the study. This is the method most widely used today.

2. Exact – This method includes expected deaths for the portion of the duration prior to the date of death but not after. This method is used to estimate the force of mortality.

3. Actuarial – This method includes the expected deaths for the entire duration where a death occurs even if the study period ends before the end of the duration.

PDF Version: Download Here

Last Revised: May 2013

Document Status: Past Exposure Draft